{kind=link}

On final week’s Animal Spirits we requested why the Fed’s aggressive charge cuts had but to interrupt something within the financial system:

Certain, the housing market is principally damaged, however the whole lot else has held up comparatively effectively…till final week that’s.

We recorded our present on Tuesday. By the weekend we might see the 2nd and third largest financial institution failures in U.S. historical past, together with the most important financial institution run we’ve ever seen.

I’ve numerous questions:

1. Is that this the Fed’s fault?

The Fed actually performed a task. It’s apparent on reflection that they held charges too low for too lengthy however they compounded that mistake by elevating charges too far too quick:

One thing was sure to interrupt by going from 0 to 60 so shortly.

Silicon Valley Financial institution executives deserve a whole lot of blame too. They mismanaged their mortgage ebook, that they had a concentrated set of shoppers and people shoppers all rushed to the exit doorways on the identical time. There are many different banks that held up simply advantageous with quickly rising rates of interest.

It’s by no means only one factor when one thing like this blows up.

The tech sector clearly doesn’t have a agency grasp on the monetary sector simply but. However the Fed has blood on its fingers right here too.

2. Is the Fed accomplished elevating charges?

It’s wonderful how shortly inflation has gone from being the most important fear to a possible afterthought. The Fed nonetheless has worth stability as a mandate and we’re not accomplished preventing the conflict on inflation.

I simply don’t see how they will stay so aggressive within the face of a banking disaster.

I don’t know if this financial institution run could have a fabric influence on the financial system nevertheless it needed to spook the Fed.

It was the failure of Continental Illinois within the early-Nineteen Eighties that made the Paul Volcker-led Fed understand they in all probability went too far with charge hikes.

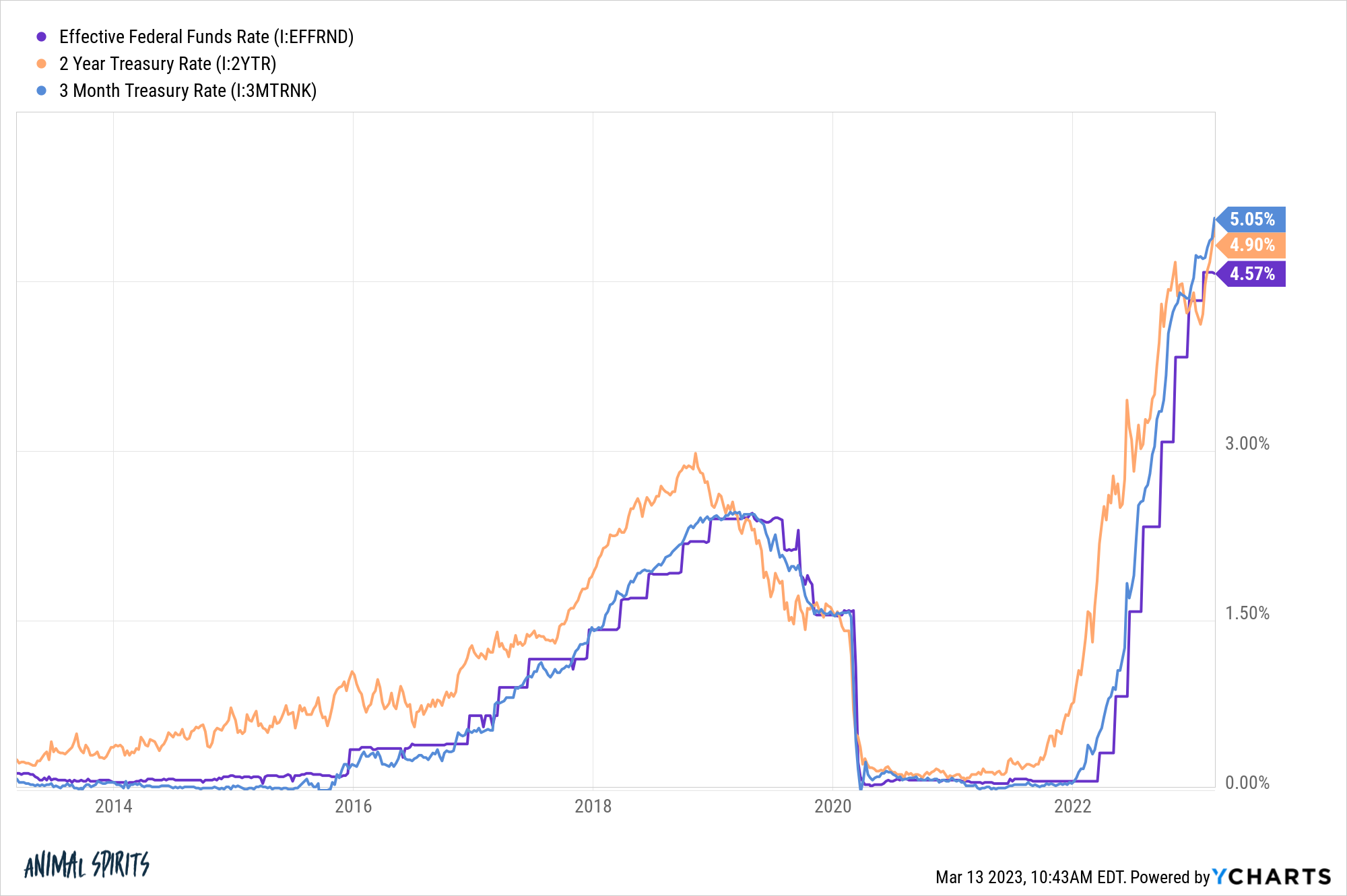

3. Why are rates of interest collapsing?

Final week the two 12 months treasury yield hit 5%. That was on Wednesday. It briefly dipped under 4% on Monday, ending the day at a bit of greater than 4%.

Charges fell throughout the board.

This could possibly be a sign from the bond market that it thinks the Fed is finished tightening (and would possibly even have to chop charges if there are extra banking issues). There’s additionally a component of a flight to security, which ought to be a welcome signal to bond traders after the drubbing mounted earnings took final 12 months.

The worst-case situation is the bond market predicting additional ache within the monetary sector and the financial system.

This all occurred so quick that the bond market itself in all probability doesn’t know for positive.

4. Is the banking business modified eternally?

The best way FDIC insurance coverage works is the banks basically pay a premium such as you would for some other type of insurance coverage.

The technical FDIC deposit insurance coverage restrict is $250,000 however the previous few days make it clear the federal government will not be going to permit depositors to lose their cash at a financial institution.

It positive looks as if meaning FDIC insurance coverage on deposits is now implicitly limitless

If that occurs the most important banks can be the most important beneficiaries as a result of they will afford it.

So whereas it could possibly be a scarcity of belief that brought on a bunch of regional banks to get their enamel kicked in on the inventory market, I believe the larger realization could possibly be that depositors will focus extra money on the larger monetary establishments.

To be truthful, inventory costs for the large banks are down too however that could possibly be as a result of the price of doing enterprise for everybody has gone up.

Sadly, I believe this implies ever worse yields for banking customers.1

5. Is a banking disaster bullish for the inventory market?

It’s weird to suppose {that a} banking disaster could possibly be bullish for the inventory market however it’s a distinct chance.

A lack of belief within the monetary system is nearly at all times deflationary. If that causes the Fed to gradual their rate of interest hikes and results in an inflation slowdown we could possibly be organising for a inventory market rally.

As at all times, that is removed from assured nevertheless it’s wild to consider how a lot the world has modified prior to now week.

Possibly this can be a blip and issues calm down nevertheless it’s onerous to place the genie again within the bottle as soon as belief within the monetary system is shaken.

6. Is know-how making the world much less steady?

I wrote on Sunday about how J.P. Morgan helped gradual the tempo of financial institution runs in 1907 by having financial institution tellers depend out buyer withdrawals very slowly.

That wouldn’t work right now.

A mixture of rumors, social media and a few panicked VCs led to greater than $40 billion of depositor withdrawals in a single day from Silicon Valley Financial institution. And people withdrawals didn’t require financial institution tellers to depend out money by hand.

They have been accomplished with the push of a button.

Expertise actually made the world extra steady throughout the pandemic nevertheless it additionally made it a lot simpler for one of many largest banks within the nation to go below in a matter of days.

As at all times, there are trade-offs with regards to innovation.

7. What are the unintended penalties of this financial institution run?

That is at all times one of many hardest inquiries to reply within the second. Typically we really feel the unintended penalties straight away and generally they’re not recognized for years down the street.

This disaster feels prefer it may result in reverberations for years to come back.

8. Is my cash secure?

It is a query lots of people didn’t suppose they needed to fear about till these previous few days. Individuals are inclined to freak out when they’re pressured to fret about issues they didn’t suppose they needed to fear about.

The excellent news is most of us won’t ever have to fret about what it’s wish to have greater than $250,000 within the financial institution however loads of enterprise homeowners do.

Placing apart the foundations which can be at the moment in place and your private emotions about ethical hazard, it’s onerous to suppose regulators and politicians would ever willingly let the banking system collapse.

And for those who personal shares, bonds, mutual funds or ETFs, no monetary establishment (assuming you’re not in Madoff Securities) can make the most of them in your behalf. If Vanguard or Constancy or Blackrock or Charles Schwab went down tomorrow for no matter motive, you continue to personal your securities. They’re merely storing them for you.

I can’t make any promise that there received’t be extra ache to come back within the banking sector as a result of religion and belief are psychological variables which can be inconceivable to forecast.

In the event you’re sitting on a complete lot of money you would possibly should be extra thoughtful about the place that money resides and the way you handle it. This ought to be a wake-up name if that’s the case.

For the remainder of us, there are many protections in place to safeguard your cash.

Additional Studying:

Financial institution Runs, Now & Then

1I financial institution with JP Morgan. Their charges are ridiculously low on deposits however I don’t ever fear about them going below. Proper or unsuitable in the event that they ever do run into bother they’re getting bailed out. I do surprise if lots of people will now really feel that means if that they had most of their cash with smaller regional banks.