{kind=link}

A reader asks:

Is it loopy to be 100% in shares from age 32 to someday in my 50s for my retirement accounts?

And one other reader asks an analogous query:

I don’t get why folks work a 30+ 12 months profession whereas investing in shares solely to glide path right into a heavier bond allocation round retirement. Why not simply keep 100% in shares, profit from share value appreciation and acquire dividends for all times?

Each of those questions happened from a latest put up I wrote that contained this long-term inventory market information:

I’m an enormous proponent of long-term pondering in the case of investing however even over the short-term the outcomes for the inventory market maintain up surprisingly effectively traditionally talking.

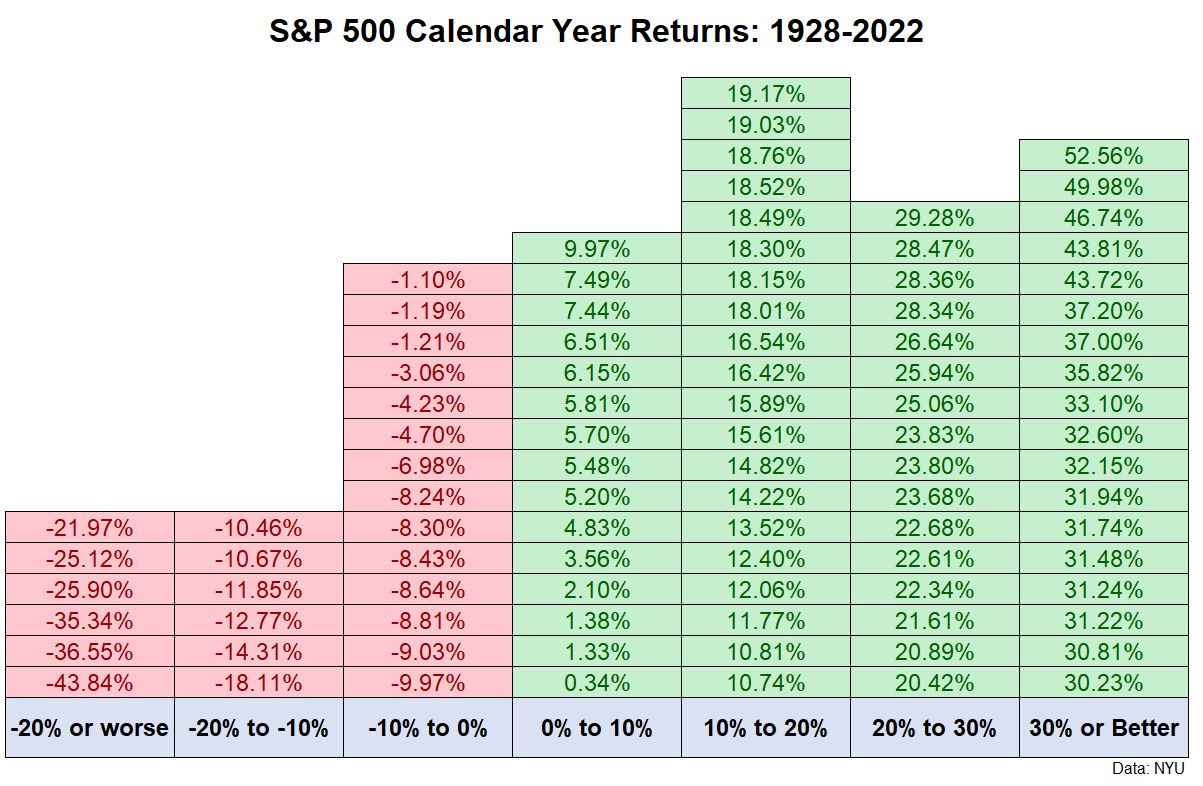

One of many craziest issues concerning the historic efficiency of the U.S. inventory market is you may have been extra prone to earn a return of 20% or extra in a given 12 months than expertise a loss.

Over the previous 95 years, there have been 34 instances when the S&P 500 has ended the 12 months with good points in extra of 20%. That’s greater than one-third of the time.

There have solely been 26 instances when a 12 months led to a loss or a bit of greater than 25% of the time.

Whenever you mix this with the truth that shares as an asset class have provided greater returns than bonds or money, it’s comprehensible that traders would query why they need to allocate to different investments.

So does it make sense to maintain 100% of your portfolio in shares?

Permit me to reply this in essentially the most finance method attainable — it relies upon.

In idea, younger folks investing for retirement ought to completely have 100% of their portfolio invested in equities.

The most important threat within the inventory market is a crash which brings decrease costs.

Your best-case state of affairs as a younger saver/investor is that you simply get to place extra financial savings to work at decrease costs. This assumes you may have the fortitude and talent to proceed saving when instances get powerful however your largest asset if you’re younger is human capital (your future incomes and financial savings energy).

Nonetheless, as you age that human capital slowly dwindles and your portfolio finally turns into your largest asset.

Most older traders allocate not less than a portion of their portfolio to money or fixed-income belongings at this level as a result of they not have as a lot time to attend out bear markets or save extra money at decrease costs.

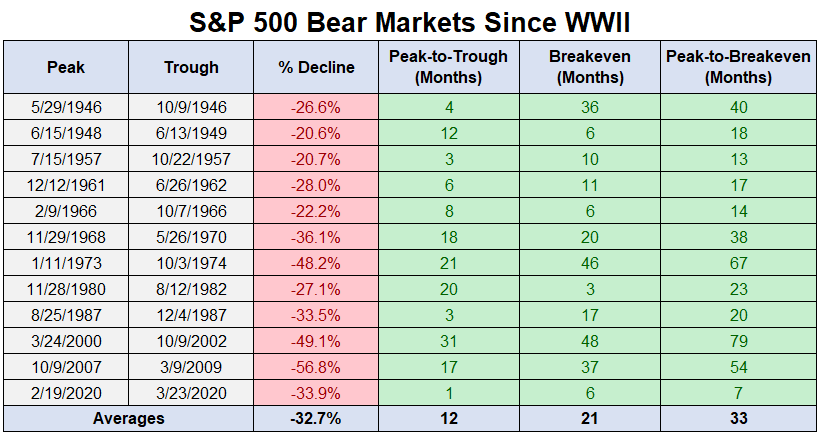

Look no additional than the historical past of bear markets to see why most traders are likely to get extra conservative as they age and their monetary belongings develop:

The common bear market lasts a few 12 months from peak-to-trough. However the common time to interrupt even is nearer to three years.

The shortest bear market in fashionable instances was the Covid crash which took simply 7 months to achieve new all-time highs once more. The longest was the 1973-94 bear market which took virtually 6 years.

That’s a very long time to be promoting off your shares when they’re down.

The entire level of switching from a mindset of accumulating wealth to preserving wealth is you don’t need to get right into a scenario the place you’re pressured to promote at a giant loss throughout a market crash. Money reserves and bonds can assist in that scenario to present your shares a while to return again.

I do perceive the will to proceed compounding your belongings even in retirement.

The easy math of compounding exhibits that almost all of your greenback good points will come later in life when you’ve constructed up a battle chest of belongings.

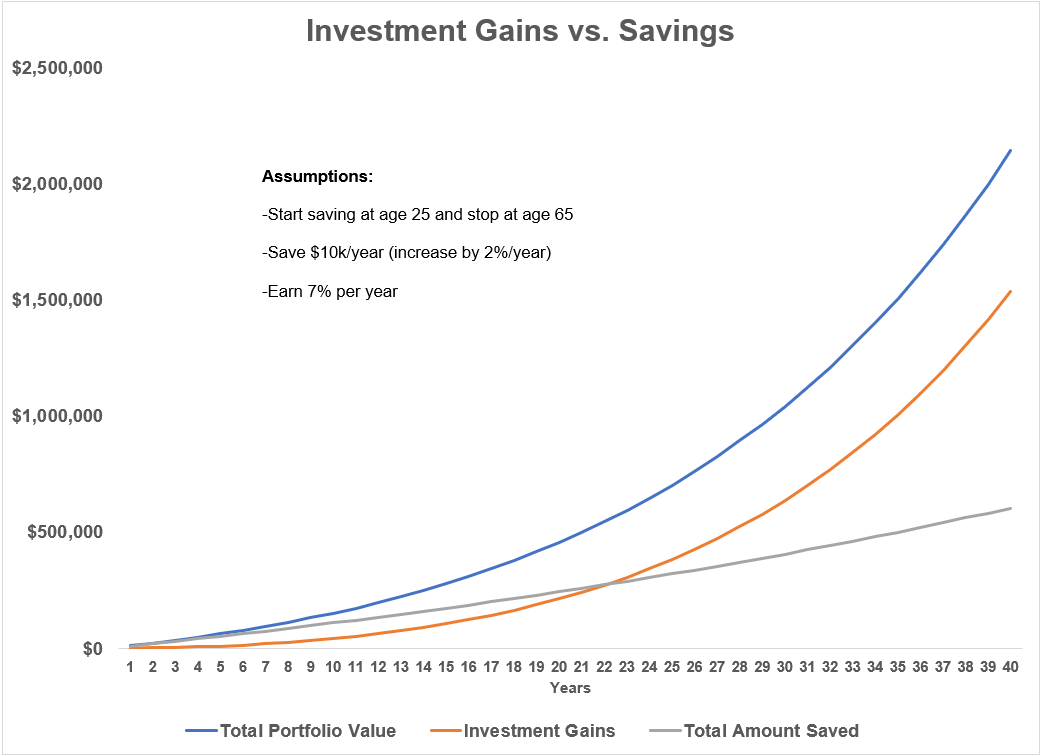

Let’s assume you begin saving $10,000 a 12 months at age 25, enhance that quantity by 2% per 12 months to account for inflation, develop your belongings at 7% per 12 months and accomplish that for 40 years if you retire by age 65.

Right here’s how issues shake out by way of saving vs. investing on this easy instance:

On this instance, your funding good points don’t overtake the whole quantity saved till age 48.

At 12 months 20, funding good points from compounding make up round 45% of the ending worth. By age 65, compounding accounts for greater than 70% of the general worth.

Saving is much extra vital the youthful you’re whereas investing issues an entire lot extra as age and construct up your financial savings.

Clearly, nobody’s precise retirement plan works out as neatly because it does on a spreadsheet. However there’s something to be mentioned about permitting your belongings to proceed compounding even when you are retired.

Like most issues in life, there are trade-offs concerned when pondering by means of this train.

The inventory market can rip your face off within the short-term however stays your greatest long-term guess when making an attempt to beat the speed of inflation over the lengthy haul.

I suppose some traders might reside off the dividends from their inventory portfolio however these money flows aren’t set in stone. The 2008 monetary disaster noticed dividends fall by greater than 31% for the S&P 500. That was far lower than the 56% crash in costs however would nonetheless be painful from a money movement perspective.

I’m 41 years previous. My retirement portfolio is 100% in shares or equity-like investments with a time horizon of effectively over a decade.

However I additionally hold a liquid reserve in money or short-term bonds for shorter-term targets, spending wants or emergencies.

I might think about that liquid reserve will develop as I strategy retirement and my time horizon adjustments however I’ll at all times have an honest allocation to shares.

The reply to the query of how a lot to maintain in shares is extra about your feelings than what finance idea says.

Some traders, even younger ones, want an emotional hedge as a result of it may be troublesome to see your life financial savings seemingly evaporate earlier than your eyes now and again within the inventory market. Others perceive the volatility concerned within the inventory market and don’t want as a lot fastened revenue to outlive.

As at all times, portfolio administration requires some steadiness between your means, want and willingness to take threat along with your cash.

There isn’t any common reply for each investor so it’s vital to assume by means of each the upside surprises (long-term compounding good points) and the draw back shocks (prolonged bear markets).

We touched on these questions and extra on the newest Portfolio Rescue:

Our tax skilled Invoice Candy joined the present once more to assist us reply questions on the tax points with early retirement, the kid tax credit score when you may have a toddler and how you can use a number of tax-deferred retirement accounts on the identical time.

Additional Studying:

Some Stuff That Most likely Received’t Occur in 2023

Podcast model right here: