{kind=link}

I’ll bear in mind this week for the remainder of my life. As an investor, you get used to inventory market volatility. Financial volatility then again has a means of sticking with you.

Within the aftermath of the pandemic, the Fed was driving an overheating financial system at 150 miles per hour. And when it realized it was going too quick, it jammed on the brake pedal as arduous because it might. For a myriad of causes, it took some time for the automotive to crash. At present it hit a wall.

Yesterday the world discovered that Silicon Valley Financial institution was coming beneath monetary strain. At present, the corporate collapsed and is now within the arms of the Federal Deposit Insurance coverage Company. The query now could be, was this a tech/startup factor, or is that this an indication of larger issues? I’ll come again to this in a minute.

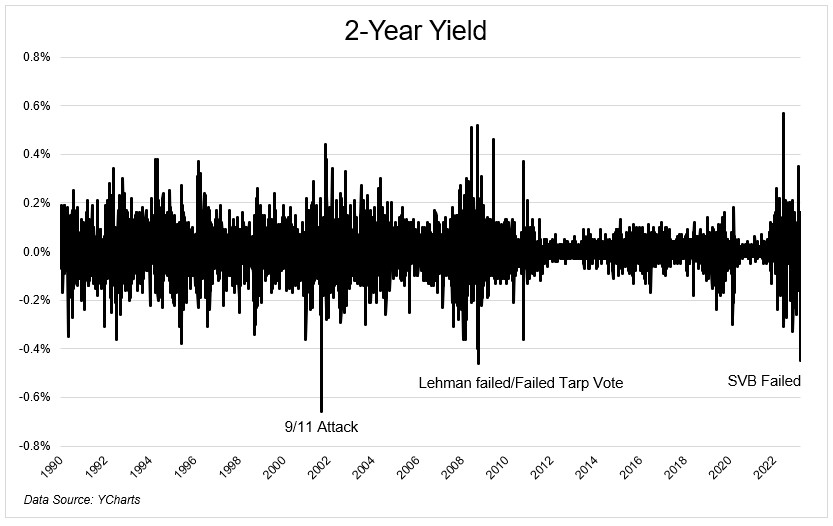

Silicon Valley Financial institution’s collapse will make all of the headlines, however what occurred within the bond market deserves numerous consideration. The two-year yield collapsed during the last two days to an extent solely seen round historic occasions (h/t Jim Bianco). Since 1990, the one different instances we noticed a decline of this magnitude was after the 9/11 assault, when Lehman Failed, when the TARP vote failed, and this week, when SVB failed.

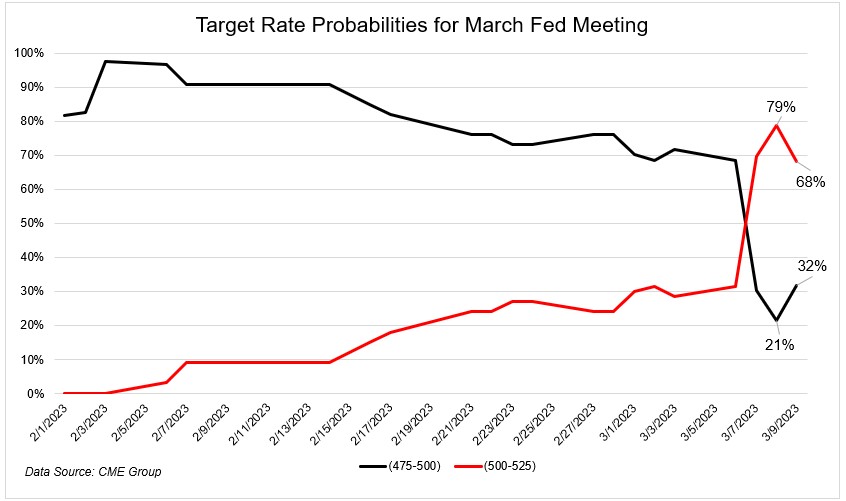

At the start of February, the market anticipated a 25 foundation level fee hike on the March assembly. After which we acquired financial knowledge that confirmed inflation and the financial system accelerating, and traders began to assume a 50 foundation level fee hike was doable.

When Powell spoke earlier within the week, the chances of fifty spiked from 30% to 79%. Now right this moment they’re again right down to 68%. That is what I imply by financial volatility. Rates of interest mustn’t commerce like a pre-revenue biotech inventory.

This factor with SVB is a really huge deal. I really feel horrible for all the businesses and people whose lives have been turned the other way up within the final 48 hours.

I don’t know sufficient to intelligently speculate on whether or not there may be something left to salvage. I’d assume that now that the financial institution run is over, there are enticing components of the enterprise that may be offered off. I’d additionally assume that the fairness is nugatory and that the depositors shall be made entire.

Returning as to if there are bigger issues to fret about, I imply, a part of me says sure. It is a large blow to confidence. Whereas SVB primarily labored with venture-backed firms, that doesn’t imply it wasn’t large. On the finish of final 12 months, they had been the sixteenth largest financial institution by deposits, behind Morgan Stanley and in entrance of Fifth Third Financial institution.

SVB is the financial institution for startups who, for essentially the most half, aren’t elevating cash anymore. In truth, they’re burning numerous it, which is without doubt one of the the reason why the financial institution discovered itself on this place. To shore up the steadiness sheet and to calm individuals down, they offered fairness to boost cash. This had the alternative impression as a result of, once more, it comes again to their buyer base. Since these are companies and never people, $250,000 of FDIC insurance coverage shouldn’t be sufficient to stop a financial institution run. Roughly 97% of deposits are over 250. So that they ran to the tune of $42 billion. The financial institution would have been okay had all people simply chilled, however that’s not how people work. Samir Kaji put this greatest, saying

What’s probably taking place: Everyone seems to be trying to run out of a burning constructing that isn’t actually burning. However within the stampede of not eager to be final out, everybody runs over the one lit candle burning, creating the blaze that doubtlessly burns the constructing down.

It is a huge deal. A variety of firms want a financial institution to, ya know, make payroll and issues like that. Pure hypothesis on my half, however I feel this factor will get mounted in a rush. Like by Monday. There’s an excessive amount of on the road.

I used to be watching Michael Santoli right this moment who made an excellent level about larger contagion. After all no one is aware of the place this goes, however at the very least right this moment, junk bonds and financial institution loans didn’t present indicators of concern. These areas of the bond market are largely pure credit score threat, they usually had been flat on the day. Once more, simply someday, however I assumed that was an fascinating commentary.

The banks then again had been buying and selling as if it weren’t only a Silicon Valley factor. The factor is, banks are so a lot better capitalized right this moment than they had been in 2008. In case your head goes there, cease it. Cease it proper now. Yea, they’re sitting at large losses on their bond portfolio, however we’re speaking treasuries for essentially the most half, not poisonous subprime rubbish.

However simply because this isn’t 2008, it doesn’t imply this isn’t unhealthy. That is unhealthy. I’m apprehensive. And I feel the fed is just too. They’ve been jamming on the breaks for the higher a part of the final two years, however solely right this moment did they slam right into a wall. Yeah, there have been layoffs in tech (not attempting to attenuate it), and sure housing exercise is down huge, however these had been gradual whereas right this moment was an occasion.

We may be experiencing a reverse Minsky second the place instability results in stability. The Fed has been attempting to interrupt issues. Mission achieved. They broke tech and housing and startups. How far more injury do they wish to do? We’re beginning to see cracks within the business actual property market too. If that goes, overlook about it.

We’ll see in just a few weeks, however I feel and I hope that this took 50 bps off the desk. Hopefully the instability that we noticed right this moment results in stability within the close to future.