{kind=link}

Berger Paints India Ltd. – Paint Your Creativeness

Berger Paints India Ltd (BPIL), integrated in 1923, is without doubt one of the main producers and sellers of paints and varnishes in India with a longtime model. It’s current in each the ornamental paint and the commercial phase, particularly, basic, automotive, protecting and powder coatings. BPIL has 24 manufacturing vegetation situated in India (together with vegetation of subsidiaries in India), Nepal, Poland, Bangladesh and Russia. It additionally has ~180 inventory stations. Its ornamental phase consists of manufacturers, comparable to Weathercoat, Luxol, Silk and Simple Clear. The Berger Group (comprising BPIL, its subsidiaries and associates and its different group firms) additionally has a global presence in eight international locations, together with Russia, Nepal, Bangladesh, and in sure international locations of Europe.

Merchandise & Providers:

Berger Paints affords a various vary of merchandise in each ornamental and industrial paint segments.

- Ornamental Paints – Inside Wall Coatings, Exterior Wall Coatings, Wooden Coatings, Steel Coatings, Enamels and Distempers beneath the manufacturers WeatherCoat, Silk, Luxol, Solitaire, and so on.

- Industrial Paints – Protecting Coatings, Powder Coatings, Marine and Container Coatings, Highway Marking Paints, Waterproofing beneath the manufacturers UltraCoat, QualiCoat, Duraberg, Epilux, House Defend, and so on.

Subsidiaries: As on FY23, the corporate has a complete of 8 Subsidiaries, 6 Step down subsidiaries and a pair of Joint Enterprise firms.

Key Rationale:

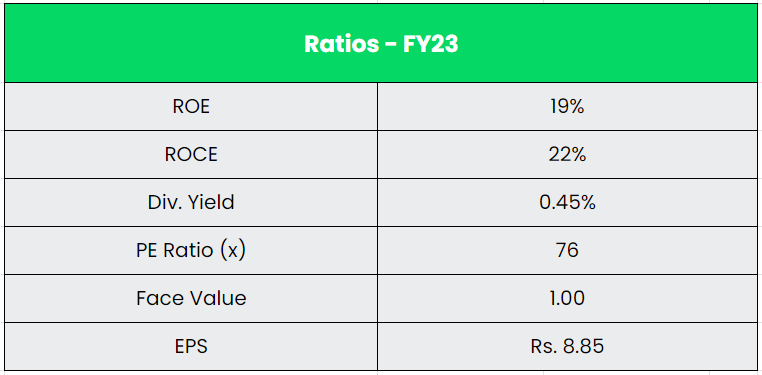

- Established Place – Berger Paints has established a formidable place within the Indian paint business, solidifying its status because the second-largest paint firm within the nation. Its success extends past nationwide boundaries, with a presence in all paint segments and a distinguished standing among the many prime 15 paint firms worldwide. In Asia, Berger Paints proudly ranks among the many prime 4 paint firms, whereas globally, it claims a spot among the many prime seven architectural (ornamental) coating firms. The corporate has been constantly enhancing its market share. In FY23, its market share stood at roughly 19.3%, in comparison with 19% in FY22 and 18.6% in FY21. Berger Paints is the market chief within the protecting coatings enterprise in India.

- Product Innovation – Berger Paints has not too long ago launched a spread of thrilling choices. Throughout Q4FY23, the corporate launched a cutting-edge product known as “antidust cool,” revolutionizing the paint business with its distinctive options. Moreover, the enlargement of the wooden coating vary has welcomed three new merchandise: Imperia Development, Imperia Breathe Simple, and Imperia Dura Coat. Capitalizing on its success, Berger Paints has skilled strong development within the premium luxurious class, spearheaded by its extremely acclaimed manufacturers, Simple Clear and Anti Mud. These manufacturers not solely lead their respective classes but in addition proceed to make exceptional progress. Nevertheless, beneath luxurious class (essentially the most premium phase), the inside luxurious product known as silk glamour, has not carried out as anticipated.

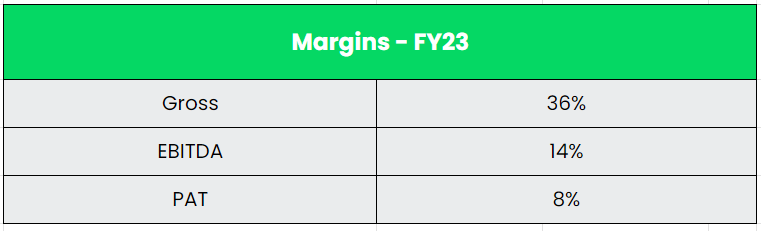

- Q4FY23 – Berger Paints achieved an honest monetary efficiency in Q4FY23. The corporate reported an 11.7% YoY enhance in income, reaching Rs.2444 crore, bolstered by a powerful 11% development in general quantity. The ornamental paints phase skilled even increased quantity development, with a powerful 14.5% rise attributed to seller enlargement and the profitable launch of recent merchandise. Whereas gross margin improved by 93 bps YoY resulting from decrease uncooked materials costs, increased working bills counteracted the profit, resulting in a decline in EBITDA margin by 170 bps YoY to 14.1%. Sadly, the corporate confronted a setback because the three way partnership firm, Berger Becker Coatings Pvt Ltd, encountered a fireplace in its Goa manufacturing unit, leading to a share of loss amounting to Rs.22 crore. So, the PAT declined 15.6% YoY to Rs.186 crore.

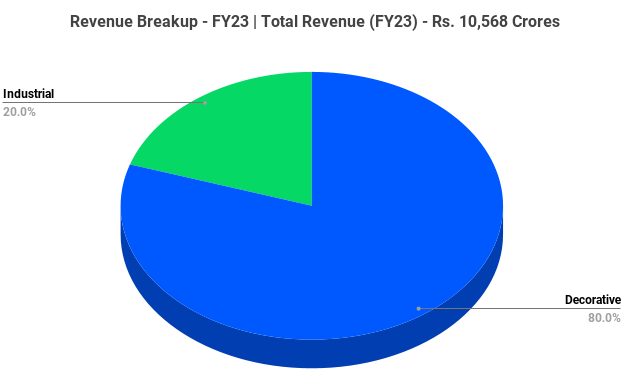

- Monetary Efficiency – The corporate’s income has multiplied practically 22 instances in a span of twenty-two years, surging from Rs.490 crore in FY01 to a powerful Rs.10,568 crore in FY23, reflecting a exceptional CAGR of 15%. Concurrently, the EBITDA has demonstrated constant development, sustaining a sturdy CAGR of 17% throughout the identical interval. FY23 marked a major milestone for the corporate, surpassing the Rs.10,000 crore income mark for the primary time in its historical past. Moreover, the protecting coatings phase celebrated a exceptional accomplishment by exceeding Rs.1,000 crore in income throughout FY23. Additionally, Berger Paints efficiently commissioned a state-of-the-art, absolutely automated manufacturing facility in Sandila, Hardoi, Uttar Pradesh. With a considerable funding of Rs.1,037 crore throughout FY 2022-23, this facility commenced business manufacturing on February 6, 2023, bolstering Berger Paints’ manufacturing capabilities.

Business:

The Indian paint business is ready to cross Rs.1 lakh crore in gross sales by 2027/28 from the present Rs.75,000 crore clocking a compounded annual development charge of 9-10%. The paint business in India is anticipated so as to add 2.5 million kilolitres of capability over the subsequent three years, which is about 20 % of the prevailing capability. The overall capex outlay for the business stands at Rs.20,000 crore, 50 % of which is able to are available from the Grasim Industries, which is investing Rs.10,000 crore. Asian Paints can also be trying to mark its presence with a capex outlay of Rs.8,000 crore. Different firms are additionally investing Rs.2,000 crore for increasing their respective capacities. The ornamental paints phase is the most important class inside the Indian paints business. It consists of inside and exterior wall paints, enamels, distempers, emulsions, and wooden coatings. This phase is pushed by elements comparable to elevated urbanization, rising disposable incomes, and rising demand for aesthetic residence decor. As a lot as 75% of the sector’s income comes from the ornamental phase and the remaining from the commercial phase. Inside ornamental, repainting accounts for 70% of income.

Progress Drivers:

- The Indian authorities has been emphasizing infrastructure growth with initiatives comparable to Good Cities Mission, Pradhan Mantri Awas Yojana (PMAY), and Atal Mission for Rejuvenation and City Transformation (AMRUT). These initiatives contain the development of roads, bridges, public buildings, and inexpensive housing, which generate substantial demand for paints and coatings.

- Because the Indian center class continues to develop, disposable incomes are growing. With increased incomes, shoppers are spending extra on residence decor, together with portray and renovation, thus driving the demand for ornamental paints.

- India is experiencing speedy urbanization, with a major rise in city inhabitants and the enlargement of cities. Urbanization results in elevated building actions, renovation tasks, and demand for paints in residential and business sectors, driving the expansion of the paints business.

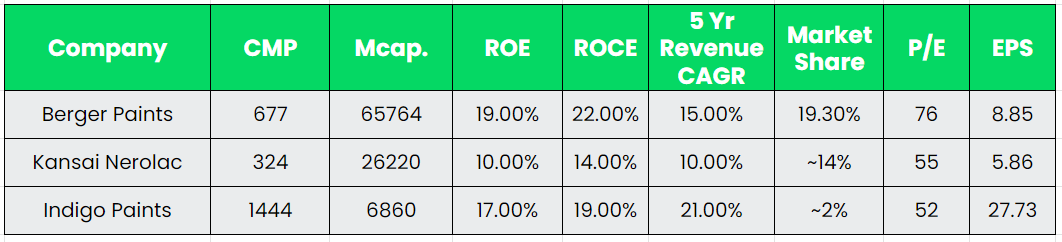

Opponents: Kansai Nerolac, Indigo Paints, and so on.

Peer Evaluation:

Berger Paints is a distinguished participant within the paint manufacturing business and holds the place of the second-largest paint producer in India, following Asian Paints. By way of monetary efficiency, Berger Paints has demonstrated spectacular outcomes that outshine its shut opponents. Furthermore, Berger Paints has strategically targeted on increasing its manufacturing capability and seller community, which bodes nicely for its future development prospects.

Outlook:

Following the commissioning of the Sandila plant, Berger Paints has skilled a major enhance in general capability, which has risen by 35% to 95,000 MT. The corporate has set a goal to attain 70-75% utilization at this plant inside the subsequent two years. Whereas some capability additions are deliberate for FY24, there aren’t any additional greenfield tasks anticipated throughout that interval. Nevertheless, the corporate has introduced plans to determine a brand new plant in Panagarh, West Bengal by March 2025. This plant will concentrate on producing industrial paints and building chemical substances. With these enlargement plans in place, Berger Paints’ administration is assured in doubling its income over the subsequent 5 years, focusing on a 15% compound annual development charge (CAGR). Presently, the corporate has 40,000 touchpoints, and it intends so as to add an extra 8,000 retail touchpoints in FY24. The administration believes that this enlargement will drive an extra 4%-5% quantity development. Berger Paints’ administration is dedicated to sustaining a gross margin vary of 38-40%, supported by benign uncooked materials costs. Moreover, they anticipate an enchancment in EBITDA margin from Q1FY24 onward and have set a steerage of 16-17% EBITDA margin within the close to time period, aided by value financial savings in areas comparable to freight prices.

Valuation:

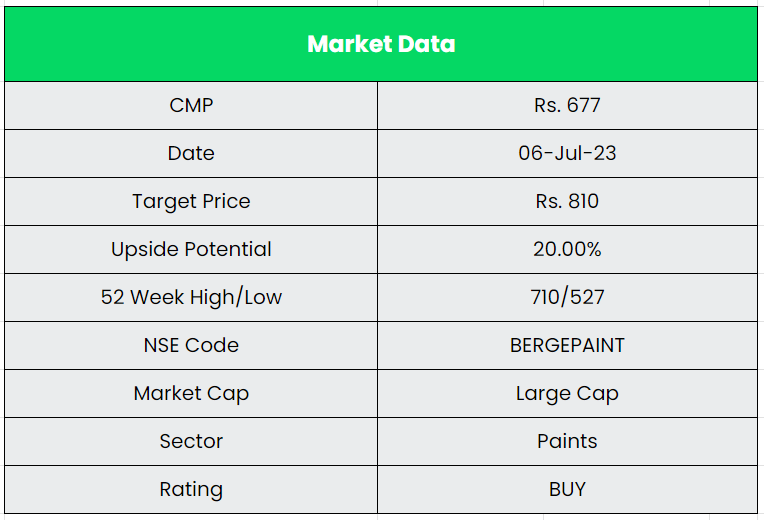

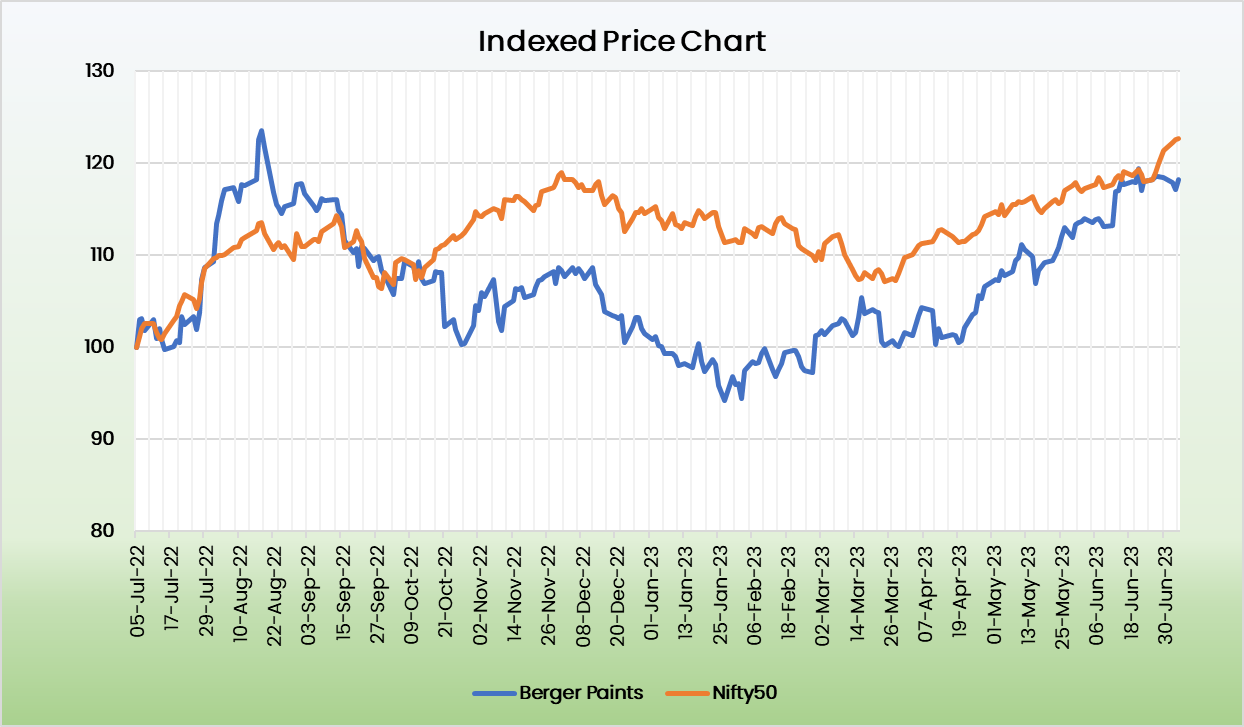

Contemplating Berger Paints’ sturdy place in each the ornamental and industrial paint segments, in addition to its capability enlargement and new product launches, it could possibly be thought of as a beautiful play within the Paint Business. We suggest a BUY score within the inventory with the goal worth (TP) of Rs.810, 60x FY25E EPS.

Dangers:

- Aggressive Danger – The Indian paint business is characterised by presence of few massive gamers within the organised phase who management important market share, whereas there are some smaller regional gamers within the unorganised phase as nicely. Entry of Grasim, Pidilite, and so on. will create a troublesome competitors among the many current organised gamers.

- Uncooked Materials Danger – The costs of uncooked supplies (account for 55-65% of complete gross sales) comparable to titanium dioxide, crude oil derivatives, pigments and resins are affected by volatility in crude oil costs which might have an effect on margins.

- Foreign exchange Danger – BPIL imports round 35% of its uncooked materials requirement, comparable to Titanium Dioxide from international locations like China, Germany, Australia, and so on. This exposes the corporate to international forex fluctuation danger along with commodity worth fluctuation danger.

Different articles it’s possible you’ll like

Publish Views:

182