{kind=link}

In the event you’re nonetheless incomes something lower than 1% in your money, it’s time to get up and do one thing…earlier than rising inflation erodes the worth of your {dollars} any additional. Listed here are some instruments you may think about using, together with low-risk and capital-guaranteed ones.

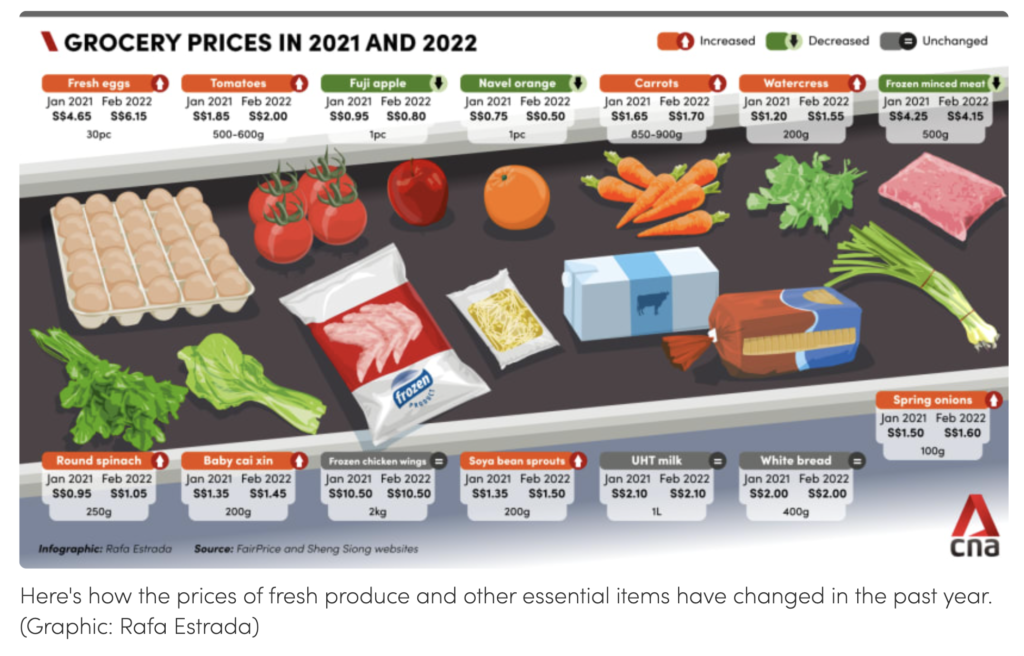

Inflation is horrifying. At first many individuals thought it will merely be momentary, given the provision chain constraints introduced on by the pandemic and afterward, the Ukraine-Russia warfare. However quick ahead to right this moment, and it’s clear that inflation isn’t going away anytime quickly. The large query now’s, what’s going to occur to our money, and the way a lot of it will likely be eroded by inflation? How a lot can we nonetheless purchase sooner or later if costs hold hovering?

For many savers, the risk-adverse and the conservative of us, investing the cash you’ve got might look like a tricky job. You are worried extra about dropping cash, however but it has gotten to the purpose the place it’s now not sufficient to stash your financial savings away both. What’s a saver to do should you don’t wish to make investments?

It troubles me to listen to that there are nonetheless loads of individuals who have but to change to one of many numerous high-yield financial savings accounts provided by our native banks, and are nonetheless retaining their cash in an account that pays solely 0.05% p.a. Being lazy is one factor, and whereas that was acceptable within the final decade, your laziness and reluctance to change will price you closely within the coming years ought to inflation ranges stay elevated.

However I can perceive – the trouble wanted to take care of a high-yield financial savings account isn’t one thing that each individual might be keen to work for, and for some of us, there are nonetheless months the place you’re unable to qualify and hit the bonus curiosity, making it a colossal waste of your efforts.

In the event you assume your time is best spent doing one thing else than to leap by way of the hoops imposed by the varied banks, then on this case, I beseech you to at the least contemplate short-term saving devices that can pay you larger than what your default checking account is providing you with.

And there are many choices, too:

Fastened deposits

In the event you like the concept of simply heading to a financial institution and signing up for a set deposit, then these are the varied choices you will get proper now:

- The shortest lock-in interval could be 1 12 months, yielding 2.85% by Financial institution of China

- The very best charge could be 3.2% for a lock-up interval of two years, provided by RHB

Singapore Financial savings Bonds

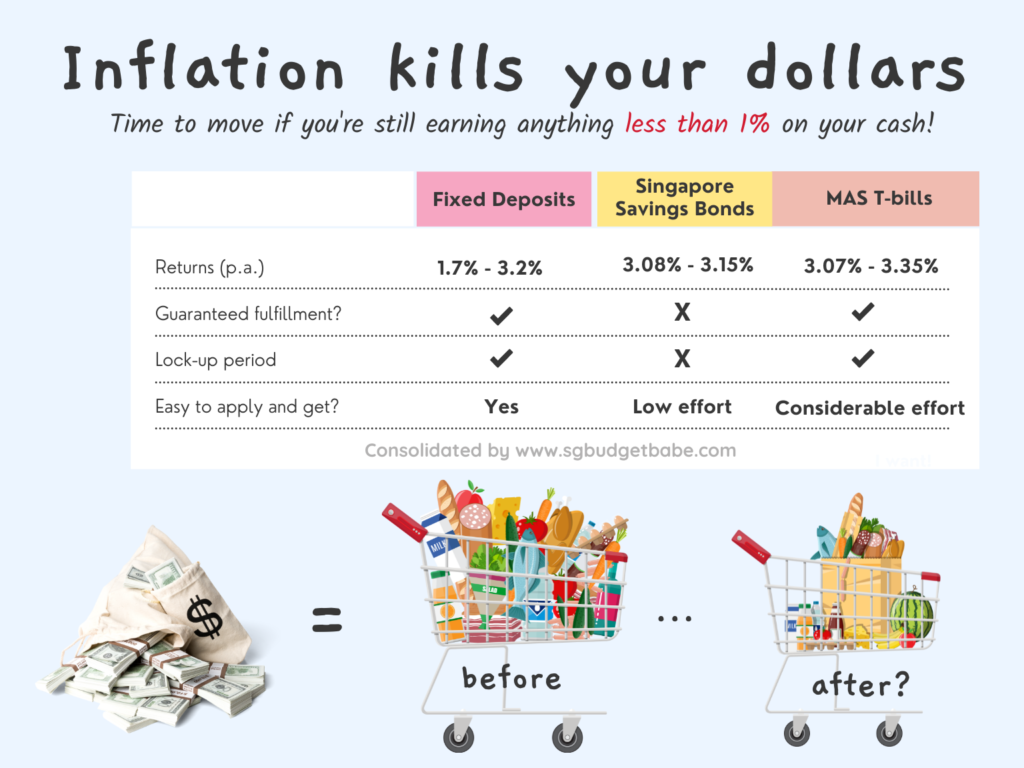

If mounted deposits aren’t your cup of tea, then what in regards to the Singapore Financial savings Bonds? It’ll take somewhat extra effort to use for them, however nothing a 10-minute analysis train (right here) will repair. Simply set your calendar reminders for the following utility date, get your money prepared, and apply on the ATM and even by way of your iBanking login, then hope that you just’ll get most allocation.

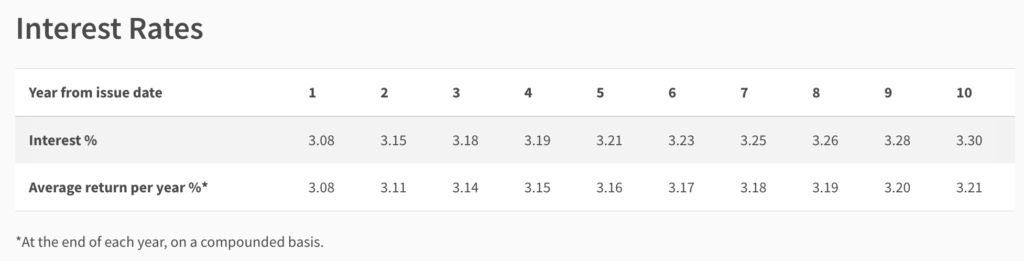

The great thing about the Singapore Financial savings Bonds is that they supply extra liquidity than mounted deposits, as you may cease and withdraw your funds throughout the following month. In the event you hold your money there for the following 2 years, you get a median return of three.11% p.a. which isn’t too shabby in any respect.

MAS T-bills

Searching for even larger yields? Effectively, should you’re keen to place in additional effort and laborious work, then the MAS T-bills is likely to be proper up your alley.

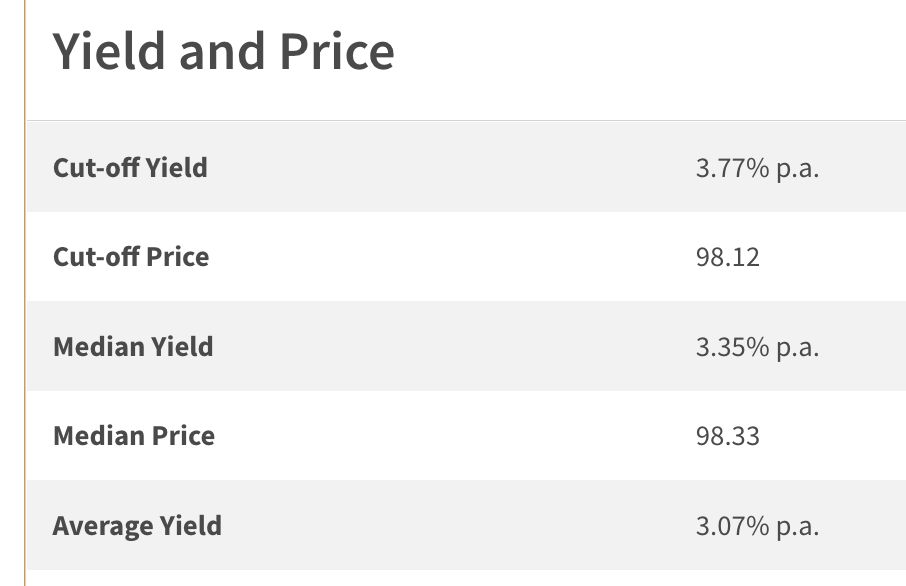

T-bills are barely extra complicated to navigate, however should you play your playing cards proper, you may probably nonetheless get the median yield of three.35% for the following 6 months, and even as much as the very best cut-off yield of three.77% should you’re actually fortunate.

The draw back? A lot of the extra enticing T-bills are just for 6 months, so you have to to repeat the method at the least twice a 12 months, and constantly look out for the applying date to be sure to make it in time earlier than it closes. Oh, and should you haven’t heard, the public sale course of is a bit more tough to navigate, so simply watch out whilst you’re executing your public sale bid.

But when the complexity places you off, there’s one final simple possibility that I can recommend: short-term mounted endowment plans.

Brief-term endowment plans

We’re no stranger to this instrument by now, and I’ve reviewed a number of first rate choices right here on this weblog as effectively. And proper now, I’ve caught wind of the truth that Nice Jap has simply launched their newest GREAT SP Sequence 9.

Disclosure: Nice Jap has kindly invited me to do a evaluate and rationalization of their newest providing, and the next part is sponsored by them.

Key Particulars:

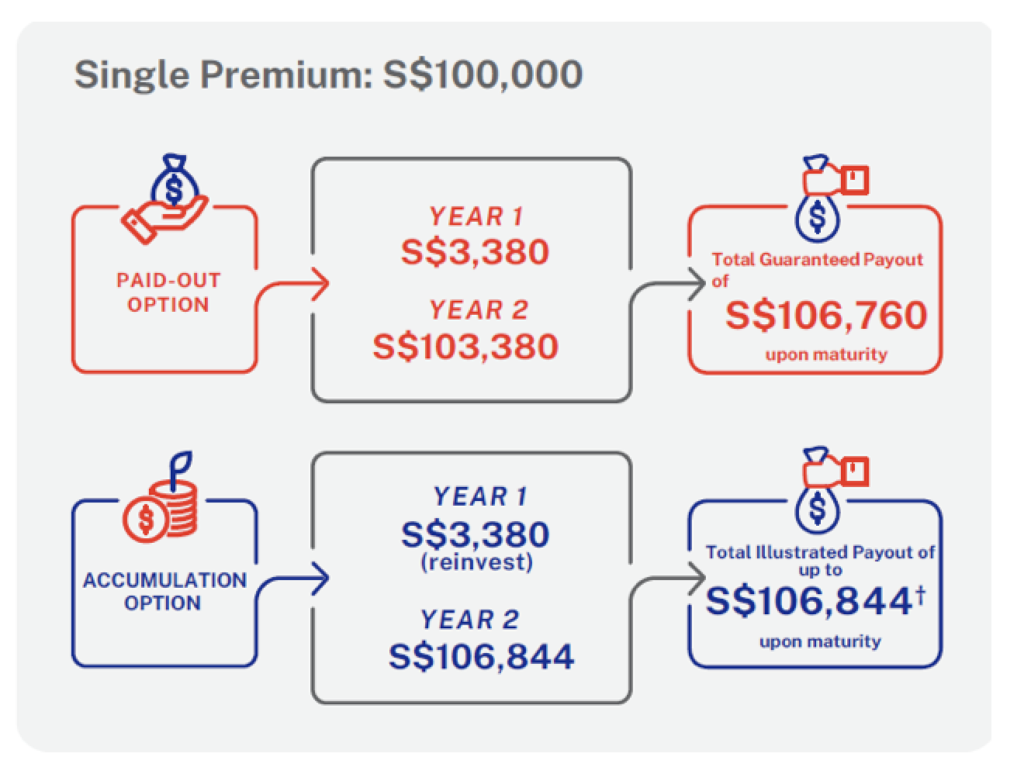

- A 2-year single premium endowment plan, with a minimal of $10,000 to use

- Assured returns of three.38% p.a*. upon maturity

- Assured payouts on the finish of every of the 2 coverage years

- Capital assured, upon maturity

- Additionally gives insurance coverage protection towards demise and whole everlasting incapacity

This might be a lovely possibility should you don’t thoughts the 2-year coverage time period.

In the event you ask me, one technique to handle this could be to place in cash you doubtless received’t want for the following 2 years, and select the buildup possibility (which reinvests your payout) so that you just’ll get larger returns on the finish of the length.

*Assured survival profit equal to three.38% of the only premium might be payable yearly on survival of the life assured on the finish of every of the 2 coverage years.

† This determine is topic to rounding and relies on the prevailing accumulation rate of interest of two.50% every year on money payout. In different phrases, should you select the buildup possibility, your first 12 months payout might be reinvested at an rate of interest of two.50% every year (not 3.38%). Based mostly on accumulation rate of interest of 1.00% every year on money payout, the overall illustrated payout at maturity is S$106,793. These charges usually are not assured and may be modified now and again.

The quantity of effort wanted? Minimal.

Software is fairly simple and you are able to do it on-line inside a few minutes. There’s additionally no want to observe altering public sale/issuance dates, monitor its progress, or fear about having to attract out your cash in 6 months – 1 12 months time and discover the following finest instrument over again to rotate it to.

As we’re in a rising rates of interest surroundings, you is likely to be pondering whether it is price getting this…what if rates of interest rise additional tomorrow?

The factor is, none of us can predict the longer term, however we will definitely take steps to develop our wealth.

What if rates of interest rise additional tomorrow?

Effectively, should you’re of the view that rates of interest might be larger from subsequent 12 months onwards, then allocate your cash accordingly between the varied choices I’ve shared up to now. You may then wish to put extra into liquid choices like SSBs, and fewer of your cash into devices like mounted deposits or Nice Jap’s GREAT SP Sequence 9.

However should you’re of the view that rates of interest might not rise considerably larger from right here, then what about doing the other? i.e. put extra into larger yielding choices – like Nice Jap’s GREAT SP Sequence 9 – which might assure you a sure stage of return, and the remainder of your cash in additional liquid choices like SSBs or T-bills so you’ve got quick access to withdraw at anytime.

Conclusion

Too many individuals are nonetheless incomes lower than 1% (or worse, simply 0.05% p.a.) on their cash right this moment, which goes to be a giant drawback quickly if they don’t get up and alter their monetary habits. With the costs of meals, electrical energy, water, mortgage rates of interest and different life-style necessities rising…can your wage rise quick sufficient to maintain up, and can your financial savings be capable of proceed offering you the extent of security that it used to have the ability to?

On the finish of the day, even for savers and the risk-adverse who aren’t eager on investing your cash, I wished to focus on that there are nonetheless loads of choices on the market that will help you cope with inflation and forestall the worth of your cash from being eroded too a lot.

It’s only a matter of what you favor. And should you’re not too positive, then I definitely assume the most recent Nice Jap’s GREAT SP Sequence 9 is price contemplating – particularly with assured returns of three.38% p.a. upon maturity.

And now, the ball is in your courtroom. Go forth and select the strategies that finest be just right for you.

Psst, such tranches are standard and have a tendency to promote out shortly, so please act quick should you’re hoping to safe a portion of this tranche for your self.

Take a look at extra particulars on GREAT SP Sequence 9 right here.

Disclosure: This submit is dropped at you in collaboration with Nice Jap, who fact-checked the supplied product details about GREAT SP Sequence 9. All opinions on this submit are mine.

The knowledge offered is for common info solely and doesn't have regard to the precise funding aims, monetary scenario or specific wants of any specific individual. As shopping for a life insurance coverage coverage is a long-term dedication, an early termination of the coverage often includes excessive prices and the give up worth, if any, that's payable to it's possible you'll be zero or lower than the overall premiums paid. You might want to search recommendation from a monetary adviser earlier than making a dedication to buy this product. In the event you select to not search recommendation from a monetary adviser, you must contemplate whether or not this product is appropriate for you. Protected as much as specified limits by SDIC. Data is appropriate as 26 October 2022. This commercial has not been reviewed by the Financial Authority of Singapore.