{kind=link}

This text was initially revealed in mint genie. Click on right here to learn it

Think about the thrill and happiness that comes from shopping for your first house. For many of us it’s an enormous step in life and a second of pure satisfaction.

However it’s additionally necessary to remind ourselves that this includes an enormous dedication financially.

This implies we have to assume by means of our choice each from an emotional and rational perspective.

So, how will we determine if it’s higher to purchase or lease your house?

Right here’s a easy framework for navigating this choice and putting the fitting stability between what you need and what is smart.

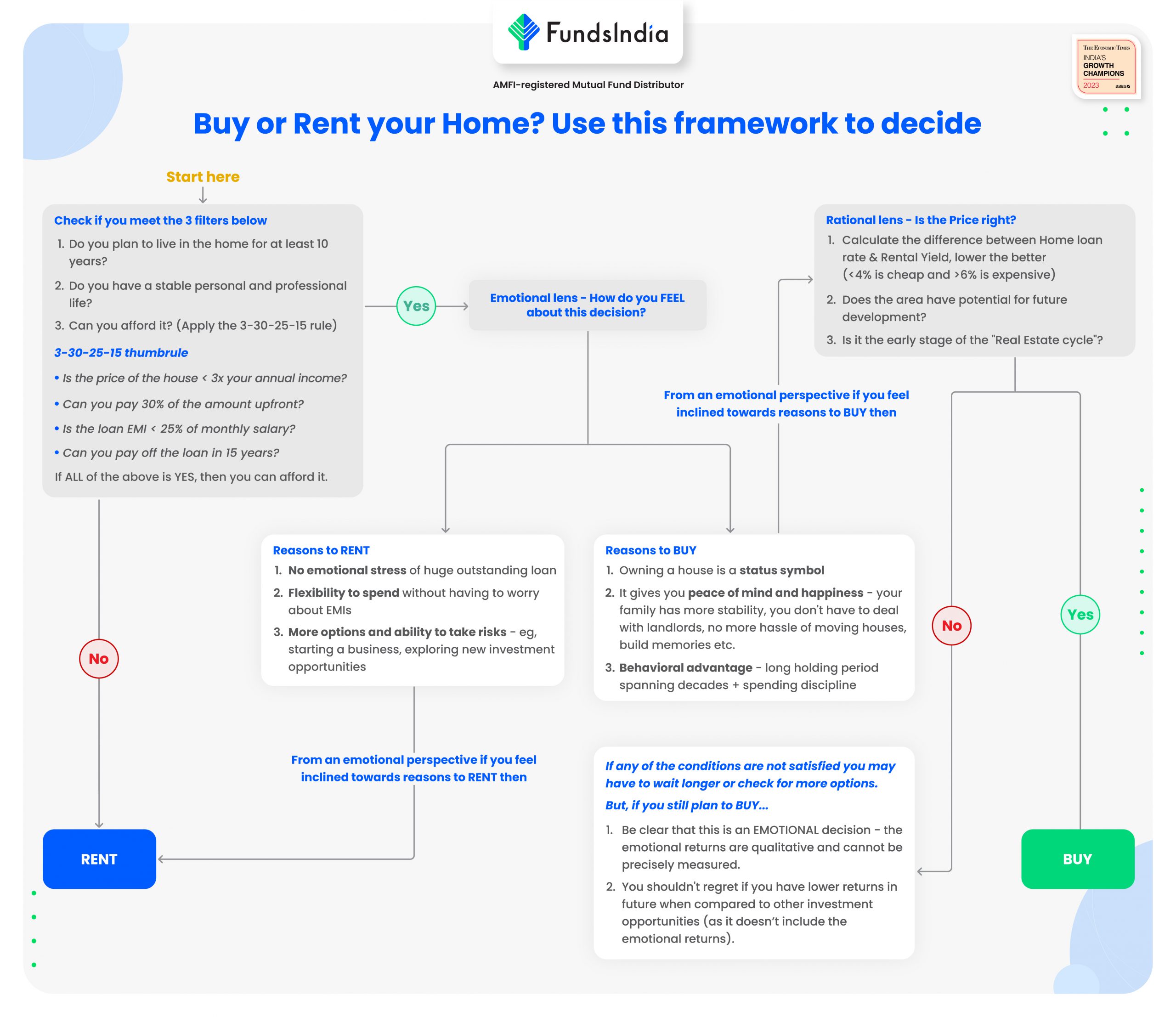

Step 1: The “3 Filter” Take a look at

Filter 1: Do you intend to reside within the house for at the very least 10 years?

When you’ve got a career which can require you to shift to a different place otherwise you need to discover different work alternatives which require you to maneuver out of the present location then it’s best so that you can RENT your house.

Filter 2: Do you could have a secure private {and professional} life?

When you’ve got an unstable job/career or an unstable private life then shopping for a house on mortgage will add to the stress. On this case it’s best so that you can RENT your house till there may be stability.

Filter 3: Are you able to afford to purchase this house?

Apply the 3-30-25-15 thumb rule to test your affordability:

- Is the worth of the home < 3x your annual revenue?

- Are you able to pay 30% of the quantity upfront?

- Is the Mortgage EMI < 25% of your month-to-month wage?

- Are you able to repay the mortgage in 15 years?

If all of the above is YES then it means you may afford to purchase the house

Determination Level:

Did you go the three filters?

- No = RENT YOUR HOME

- Sure = Transfer to the following Step

Step 2: Emotional Lens – How do you FEEL about this choice?

Emotional Causes to RENT

- No emotional stress of an enormous excellent house mortgage

- You’ve the flexibility to spend effectively and should not have to fret about EMIs

- You’ve extra funding choices and increased capability to take dangers.

Eg: beginning your individual enterprise, exploring new funding alternatives and so on.

Emotional Causes to BUY

- Proudly owning a home is a standing image and indicators to others that you’re profitable

- It provides you peace of thoughts and happiness – your loved ones has extra stability, you don’t should take care of landlords, no extra problem of shifting homes, you construct recollections and so on.

- Behavioral benefit – inculcates the behavior of saving (EMIs), controls spending, and self-discipline to carry the asset for a very long time (spanning many years).

Determination Level:

- In case you really feel inclined in the direction of causes to lease = RENT YOUR HOME

- In case you really feel inclined in the direction of causes to purchase = Transfer on to the following Step

Step 3: Rational Lens – Is the Value Proper?

Now the next step is to search out out if the worth of the home is true. These three vantage factors will allow you to do this

- Is it low cost or costly?

As a way to decide whether or not the worth of the home is affordable or costly, you may examine the Residence Mortgage price and the Rental yield.

Rental Yield is the Annual Rental Revenue (you can get in the event you lease it out) as a Share of Home Value.

Rental Yield = Annual Lease ➗ Value of the home

In the case of rental yields, increased the higher!

Now, calculate the distinction between house mortgage price and rental yield.

Decrease the distinction, the higher.

- Residence mortgage price – Rental yields < 4% = CHEAP

- Residence mortgage price – Rental yields > 6% = EXPENSIVE

Right here is an instance of how this works,

Assume the worth of the home is Rs 1 crore and the month-to-month lease is Rs 20,000 (so yearly it’s Rs 2.4 lakhs) and your present house mortgage price is 9% .

Rental yield = 2.4% (Rs 2.4 lakh ➗ Rs 1 crore)

Residence mortgage price 9% – Rental yield 2.4% = 6.6%

This implies the worth is dear proper now.

- Is there potential for future improvement in your chosen space?

A property’s return potential is extremely depending on its location, neighborhood, facilities, connectivity, and future improvement prospects.

This contains

- Present entry to services like places of work, faculties, hospitals, malls and markets, and transportation hubs

- Connectivity to main roads, highways, and public transportation and so on.

- Future developments like deliberate public or non-public infrastructure tasks, metro rail, flyovers, faculties, markets, hospitals and so on

These components will allow you to assess the scope for future improvement when buying actual property.

- The place are you in the actual property cycle?

Understanding the actual property cycle is necessary to know if the worth is true and what to anticipate as future appreciation. Actual property costs sometimes expertise cycles characterised by a interval of upward momentum lasting 7-10 years, adopted by a subsequent downturn.

So, ‘WHEN’ you enter the actual property cycle is a key determinant of your long run returns.

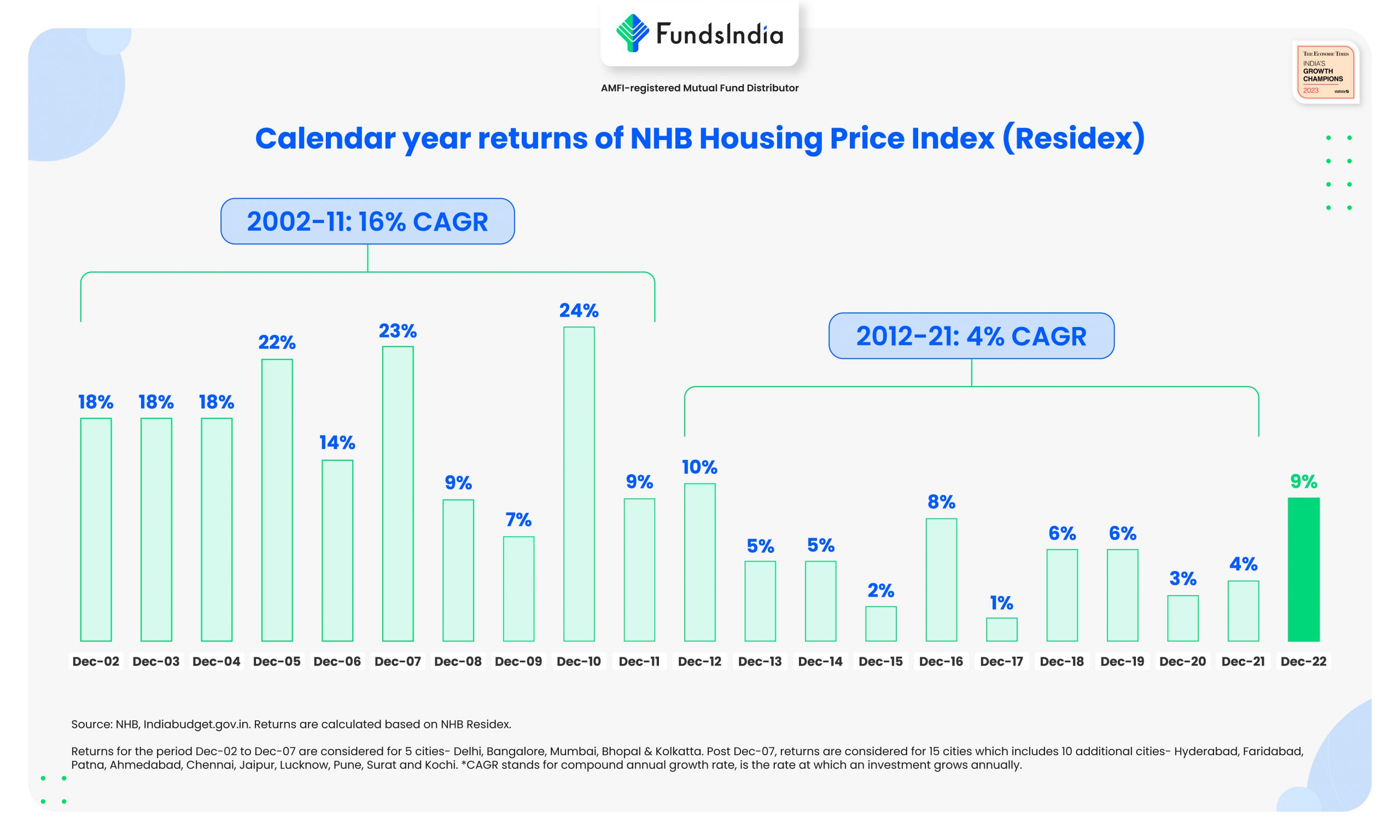

Within the chart under we are able to see the final 20 years returns from an funding in actual property,

2002-2011 – 16% annualized returns (up-cycle)

2012-2021 – 4% annualized returns (down-cycle)

As seen above, it’s higher to purchase on the early levels of the actual property cycle

How do we all know it’s the early levels of the following up-cycle?

Listed below are some components to establish this

- Low Previous Returns – if the costs have been stagnant (time correction) or declined over the past 7-10 years. Examine for early indicators of a worth decide up.

- Low Provide – Unsold stock is lowering and there are few or no new actual property challenge bulletins.

- Low Residence Mortgage charges – If house mortgage charges are low in comparison with the final 20 12 months historical past

- Enhancing Demand – led by higher affordability – increased salaries, decrease rates of interest and decrease home costs

Collectively, these components present a sign of the early stage of an up-cycle.

Briefly, the worth is true if

- The distinction between house mortgage price and rental yields doesn’t exceed 6% (>6% is dear)

- The realm has potential for future improvement and worth appreciation

- You’re investing on the early stage of the actual property cycle

If any of the above situations will not be met, then it means the worth will not be proper.

So, what occurs when the worth will not be proper?

You’ll have to WAIT LONGER to purchase the fitting property or look out for MORE OPTIONS with the RIGHT PRICE.

However, even when the worth will not be proper and you continue to need to purchase a home, what to do?

Bear in mind this,

- Be clear that that is now an EMOTIONAL choice – the emotional returns are qualitative and can’t be exactly measured.

- You shouldn’t remorse if you find yourself with decrease returns in future when in comparison with different funding alternatives (because it doesn’t embody the emotional returns).

When you come to phrases with the above two realities, you may go forward and nonetheless purchase the house although the worth will not be favorable

Summing it up… Visually!

An outline of this easy framework will be discovered within the visible flowchart under.

Different articles chances are you’ll like

Put up Views:

284