{kind=link}

Life is filled with surprises. Whether or not in private, skilled, or monetary issues. Nonetheless, if we don’t be taught from our errors, we’re committing against the law in opposition to ourselves. Because of this, let me share a couple of classes I’ve realized in 2022.

Nifty was round 13,700 final 12 months. In 2020, we skilled a fall brought on by Corona. Because of this, the uptrend from round 8,000 Nifty ranges in 2020 to round 13,700 in December 2021 instilled huge confidence in us that the worst was over and we now solely needed to face the uptrend. The truth, nonetheless, is kind of completely different.

Monetary Classes from 2022

# Nothing is PERMANENT

As beforehand said, the Nifty fell roughly 27% from its peak of 12,256 on round tenth January 2020 to eight,083 on round third April 2020. It took roughly 6-7 months to achieve the earlier degree, and it then peaked at 18,338 on October 14, 2021. Huge 45% uptrend from the autumn.

This instilled an excessive amount of confidence in us that going ahead Indian or international economies at the moment are within the midst of a multi-year or multi-decade bull run.

NONE, nonetheless, predicted the Ukraine battle or the worldwide inflation affect. Due to these elements, we’re virtually a 12 months right into a sideways market. Trying again on the Nifty chart from final 12 months, we will see that the uptrend is round 7.3%. For individuals who noticed a implausible uptrend of almost 45% from the Covid fall to final 12 months’s finish degree, it could look like ridiculous returns.

The reality, nonetheless, is that NOTHING IS PERMANENT. Neither BULL nor BEAR markets.

# FOMO (Worry Of Lacking Out) creates extra errors

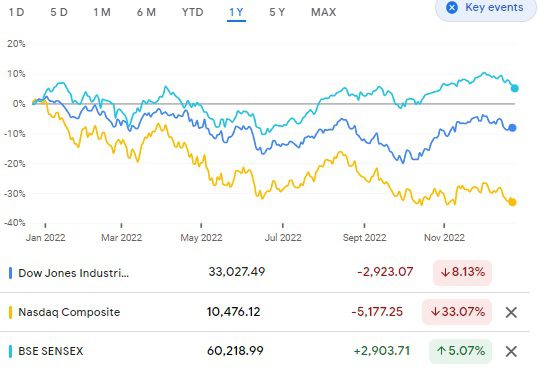

Investing in US shares turned fashionable after Covid. Principally due to how the US market behaved on the time. In reality, if you happen to don’t make investments, you’re handled like a DUMB. A lot of our new purchasers used to ask why we didn’t advocate investing within the US fairness market. Nonetheless, as beforehand said, this FOMO phobia fades progressively because the US market crashes extra dramatically than the Indian marketplace for a 12 months.

The under photos gives you readability.

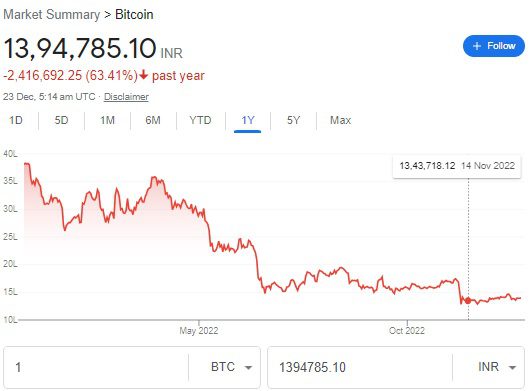

The identical is the story of Crypto.

In reality, I used to be against Crypto investing and at all times requested those that invested or had been keen to take a position, “If one thing went flawed with the market or platform suppliers, who do you method?” Why take an pointless danger when the reply is NONE?

Many individuals are unaware of the prices related to investing in shares in america. Therefore, I wrote an in depth publish on that “Learn how to put money into US Shares from India?“. Many individuals blindly adopted US inventory investing and cryptocurrency. When you may have FOMO phobia, you discover that you just make a variety of errors.

# Emergency won’t ask in your permission

I misplaced a buddy and classmate who by no means approached me for monetary recommendation and didn’t cowl the basics similar to time period life insurance coverage, medical health insurance, an emergency fund, or unintentional insurance coverage. He died of cardiac arrest, leaving his spouse with two young children. He solely had a couple of LIC insurance policies, one loan-free flat, and one or two plots of land.

Simply think about the state of affairs of a household. They’ve to think about present ongoing bills and in addition the children’ future.

Life is filled with unknowns. That’s the reason the next quote is good for getting ready for such surprises.

“Hoping for the very best, ready for the worst, and unsurprised by something in between.” —Maya Angelou

We can not predict financial downturns, fatalities, medical emergencies, or job loss. Nonetheless, the one factor we will do is put together. When such emergencies strike, the magnitude is unknown to us.

# All belongings have BEST and WORST days

Contemplate historical past. You will have observed that Gold (refer our publish “Gold Volatility – Primarily based on 43 Years of Historical past“) is unstable. For a couple of years, it might be actual property and gold, after which it might be fairness. Because of this, we’re uncertain which asset class will carry out higher sooner or later. NOBODY can predict. Concentrating on a single asset class in such a state of affairs is extraordinarily dangerous. Diversification, alternatively, is a mantra.

In reality diversification just isn’t new to us. Once I was studying John Bogle’s guide “Frequent Sense on Mutual Funds”, I first got here throughout “The Talmud Portfolio”. The Talmud is a set of Jewish texts beneath the class of the Oral Torah. The Jerusalem Talmud was printed round 350–400 CE, whereas the extensively cited Babylonian Talmud was printed about 500 CE. The 2 elements that make up the Talmud are the unique supply or Mishnah, and the Gemara (which is written in Aramaic and consists of further writings that broaden on the matters mentioned within the Mishnah).

One such on-line model of Bava Metzia 42 as “Rebbi Yitzchak advises an individual to take a position his cash – one-third in land and one-third in enterprise, and the remaining third, he ought to maintain in money.”

Nonetheless, we ignore such fundamentals of investing. Primarily due to the frenzy to create wealth fastly and in search of BEST and most COMPLICATED product served to make use of by the hungry monetary trade.

# Small Steps with CONSISTENCY matter rather a lot

On daily basis, I stroll 8-10 kilometers. Assume that if I skip 65 days in a 12 months (on account of private, well being, or climate points), then 300 days 10 km a day means I walked round 3000 km in a 12 months. Greater than the gap between Bangalore and Delhi!!

Equally, if you happen to apply the idea of studying 5 pages per day (which takes not more than half-hour of your time), you’ll find yourself studying 1,825 pages per 12 months. If we assume that every guide is round 200 pages lengthy, you should have learn 9 books in a 12 months.

I’m utilizing these examples as a result of I do these two issues each day. You possibly can, nonetheless, develop your individual habits that can profit you personally, professionally, and financially.

Do not forget that in in the present day’s world, FOCUS is extra essential than IQ or EQ. Use this in your private finance. Start by making small adjustments daily and wait a couple of years or many years to see the outcomes.

First, I used well being for instance. Principally as a result of small adjustments to your well being could make an enormous distinction in the long term. In any case, what good is wealth if you happen to don’t have good well being?

Please share your learnings too if they’re attention-grabbing. On the finish, I firmly consider in mutual studying 🙂