{kind=link}

In the present day we’ll talk about the important thing variations between a mortgage co-borrower and a mortgage co-signer.

Whereas the 2 phrases sound fairly comparable, and are typically used interchangeably, there are essential distinctions that you need to be conscious of it contemplating both.

In both case, the presence of a further borrower or co-signer is probably going there that will help you extra simply qualify for a house mortgage.

As an alternative of relying in your earnings, belongings, and credit score alone, you possibly can enlist assist out of your partner or a member of the family.

This may occasionally mean you can qualify for a bigger mortgage quantity, snag a decrease rate of interest, and even win a bidding conflict through a stronger supply.

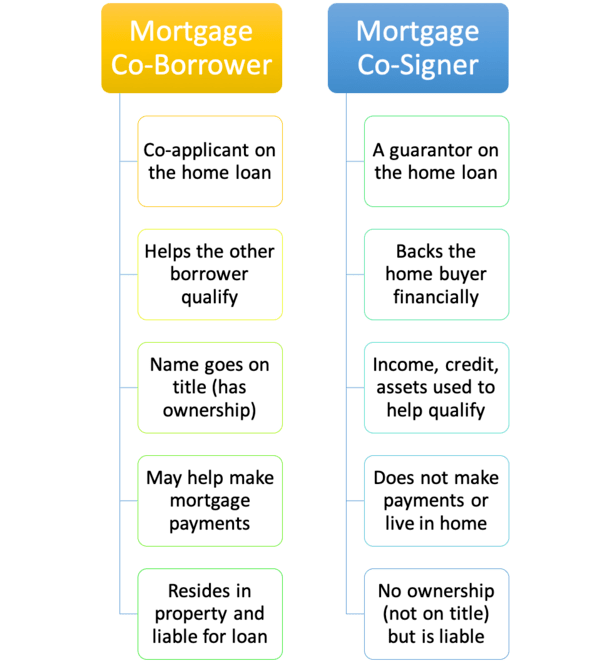

What Is a Mortgage Co-Borrower?

A mortgage co-borrower is a person who applies for a house mortgage alongside the primary borrower.

Sometimes, this may be a partner that may even be dwelling within the topic property. To that finish, they share monetary accountability and possession, and are each listed on title.

For instance, a married couple might resolve to buy a house. They apply collectively as co-borrowers.

Doing so permits them to pool collectively their earnings, belongings, and credit score historical past. Ideally, it makes them collectively stronger within the eyes of the lender and the house vendor.

This might imply the distinction between an permitted or rejected loa utility, and even a successful vs. shedding bid on a property.

Simply think about a house vendor who’s deciding between two competing bids with their actual property agent.

Do they go along with the borrower simply scraping by financially, or the married couple with two good jobs, two regular incomes, stable pooled belongings, deep credit score historical past, and many others.

Talking of that earnings, two incomes may permit you afford extra house.

What Is a Mortgage Co-Signer?

A mortgage co-signer is a person who acts as a guarantor on a house mortgage and takes accountability for paying it again ought to the borrower fail to take action.

In that sense, the co-signer acts as a type of security web, and never an energetic participant.

This implies they don’t make month-to-month funds, nor do they reside within the topic property.

Maybe extra importantly, they don’t have possession curiosity within the property. Nonetheless, they share legal responsibility together with the borrower(s).

To be blunt, they get all of the potential unhealthy with none of the great, i.e. possession.

However the entire level of a co-signer is to assist another person, so it’s not about them. A typical instance is a mother or father co-signing for a kid to assist them purchase a house.

Each their earnings and credit score historical past can come into play to assist their youngster get permitted for a mortgage.

For the file, somebody with possession curiosity within the property can’t be a co-signer. This contains the house vendor, an actual property agent, or house builder. That might be a battle of curiosity.

Mortgage Co-Borrower vs. Mortgage Co-Signer

What Is the Credit score Rating Affect for Co-Debtors and Co-Signers?

As a co-signer, you’re liable for the mortgage for your complete time period, or till it’s paid off through refinance or sale.

This implies it’ll be in your credit score report and any unfavourable exercise (late funds, foreclosures) associated to the mortgage will carry over to you.

There are additionally credit score inquiries, although these normally have a minimal impression.

Nonetheless, it’s attainable the on-time mortgage funds will help you credit score over time, per Experian.

The opposite situation is it could restrict your borrowing capability in case you’re on the hook for the mortgage, even in case you don’t pay it.

Its presence may make it tougher to safe your personal new traces of credit score or loans, together with your personal mortgage, if wished, attributable to DTI constraints.

When you’re a co-borrower on a mortgage, credit score impression would be the similar as in case you had been a solo borrower. There might be credit score inquiries when making use of for a mortgage.

And the mortgage will go in your credit score report if/when permitted, and fee historical past might be reported over time.

On-time funds can enhance your rating, whereas missed funds can sink your rating.

What A couple of Non-Occupant Co-Borrower?

You may additionally come throughout the time period “non-occupant co-borrower,” which because the identify implies is a person on the mortgage who doesn’t occupy the property.

On high of that, this particular person might or might not have possession curiosity within the topic property, per Fannie Mae.

This differs from a co-signer, who doesn’t have possession curiosity as indicated on title.

However each should signal the mortgage or deed of belief, and could have joint legal responsibility together with the borrower.

On FHA loans, a non-occupying co-borrower is permitted so long as they’re a member of the family with a principal residence in america.

If not a member of the family, or for 2-4 unit properties, a 25% down fee is required (max 75% LTV).

Both method, the non-occupant co-borrower takes title to the property, not like a co-signer who doesn’t.

Notice that co-signers or non-occupant co-borrowers are usually not permitted on USDA loans.

And for VA loans, a co-signer have to be a partner or energetic obligation/veteran who resides within the property.

Most lenders don’t permit non-occupying co-borrowers on VA loans, although a “joint mortgage” could also be an choice.

When To not Use a Co-Borrower for a Mortgage

Consider it or not, there are occasions when utilizing a co-borrower may do extra hurt than good.

The most typical instance is when the possible co-borrower has poor credit score, and even marginal credit score.

As a result of mortgage lenders sometimes contemplate all debtors’ credit score scores after which take the decrease of the 2 mid-scores, you gained’t need to add somebody with questionable credit score (except you completely need to).

For instance, say you might have a 780 FICO rating and your partner has a 680 FICO rating. You propose to use collectively as a result of they’re your partner.

However then you definitely discover out that the mortgage lender will qualify you on the 680 rating. That pushes your mortgage price method up.

On this case, it’s possible you’ll not need to use the co-borrower except you want them for earnings functions.

They’ll nonetheless be on title and get possession within the property with out being on the mortgage.

How a Co-Borrower’s Greater Credit score Rating Can Make You Eligible for a Mortgage

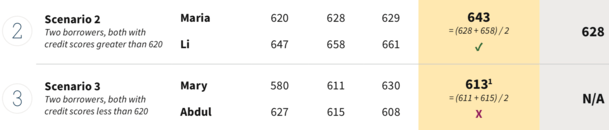

Not too long ago, Fannie Mae instituted a brand new methodology for figuring out eligibility when there’s a co-borrower.

They take the median rating of every borrower and mix them, then divide by two (the common).

For instance, think about borrower 1 has scores of 600, 616, and 635. They’d sometimes use the 616 rating and inform the borrower it’s not ok for financing.

Now suppose there’s a co-borrower (borrower 2) with FICO scores of 760, 770, and 780.

Fannie Mae will now mix the 2 median scores (770+616) and divide by two. That might lead to a mean median credit score rating of 693.

This permits borrower 1 to adjust to Fannie/Freddie’s minimal 620 credit score rating requirement (for conforming loans).

Notice that that is only for qualifying, and provided that there’s a co-borrower. And it doesn’t apply to RefiNow loans or manually underwritten loans.

Moreover, pricing (and mortgage insurance coverage if relevant) remains to be decided by the consultant credit score rating (616).

So collectively you qualify, however the mortgage price could be steep based mostly on the decrease credit score rating used for pricing.

Notice that not all lenders might permit a borrower to have a sub-620 credit score rating, no matter these tips (lender overlays).

Easy methods to Take away a Mortgage Co-Borrower or Co-Signer

Whereas it may be good to have a mortgage co-borrower or co-signer early on, they could need out in some unspecified time in the future.

There are a number of explanation why, probably a divorce, probably to unencumber their very own credit score.

Fortuitously, it may be completed comparatively simply through a conventional mortgage refinance.

The caveat is that you just’d have to qualify for the brand new house mortgage with out them. Moreover, you’d need mortgage charges to be favorable at the moment as effectively.

In any case, you gained’t need to commerce in a low-rate mortgage for a high-rate mortgage merely to take away a borrower or co-signer.

A typical state of affairs could be a younger house purchaser who wanted monetary help early on, however is now flying solo.

They might refinance and alleviate the attainable stress/monetary burden of the co-signer and at last stand on their very own.

Options to Utilizing a Co-Borrower/Co-Signer

When you’re unable to discover a prepared co-borrower or co-signer to go on the mortgage with you, there could be options.

First, decide what the difficulty is, whether or not it’s a low credit score rating, restricted earnings, or an absence of belongings.

These with low credit score scores might need to contemplate bettering their scores earlier than making use of. Apart from making it simpler to get permitted, you could possibly qualify for a a lot decrease rate of interest.

These missing earnings/belongings can look into choices that require little to no down fee.

For instance, each VA loans and USDA loans don’t require a down fee.

There may be additionally Fannie Mae HomeReady and Freddie Mac House Potential, each of which require simply 3% down and permit boarder earnings (roommate) to qualify.

Or inquire about grants and down fee help through an area lender or state housing company.

There are numerous mortgages that require little or no down and subsequent to nothing by way of belongings/reserves.

You may additionally contemplate decreasing your most buy worth if these points persist.

An alternative choice is utilizing reward funds to decrease your LTV ratio and mortgage quantity, thereby making it simpler to qualify for a mortgage.