{kind=link}

Main as much as 2022, monetary advisors and their purchasers had grown accustomed to a comparatively low mortgage fee atmosphere. Actually, till earlier this yr, the common 30-year fastened mortgage fee had stayed under 5% since 2010 (and under 7% since 2001). However because the Federal Reserve has sought to boost rates of interest this yr to fight inflation, mortgage charges have reached increased ranges not seen in additional than 20 years, with 30-year fastened mortgages reaching a mean of 6.9% in October 2022, twice the three.45% common fee in January.

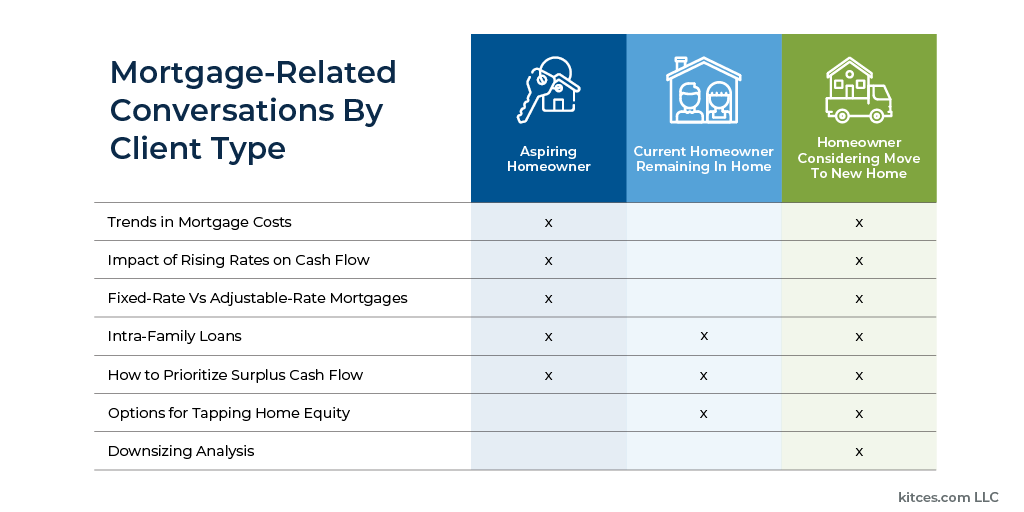

Whereas the plight of immediately’s first-time homebuyers dealing with increased mortgage charges has attracted a lot media consideration (deservedly so, because the month-to-month cost on a 30-year fastened mortgage for the median-priced house within the U.S. elevated by almost $1,000 prior to now yr), increased rates of interest can have an effect on monetary planning calculations for present owners as properly. For example, increased rates of interest have raised the borrowing prices for these trying to faucet their house fairness by way of a house fairness mortgage or a Residence Fairness Line Of Credit score (HELOC), and older owners contemplating a reverse mortgage may even be topic to increased rates of interest.

On the similar time, increased rates of interest can current alternatives for some people. For instance, those that are concerned with making an intra-family mortgage may generate extra earnings from the upper Relevant Federal Charges (whereas the mortgage recipient advantages from a fee considerably decrease than customary mortgage charges). As well as, many present owners may have mortgages with charges decrease than the ‘risk-free’ fee of return now obtainable on U.S. authorities debt, which has risen alongside broader rates of interest (maybe altering the calculus of whether or not to pay down their mortgage early). And present owners with vital fairness may contemplate downsizing and shopping for a smaller house in money, doubtlessly benefiting from a less-competitive housing market without having to take out a mortgage on the present charges.

In the end, the important thing level is {that a} increased interest-rate atmosphere impacts not solely homebuyers trying to buy a house for the primary time but additionally those that are present owners. Additional, given {that a} house may be thought-about a consumption good (that always comes with emotional attachments) in addition to an asset on the house owner’s internet price assertion, advisors can even add worth by serving to purchasers discover their home-related objectives and assessing the monetary tradeoffs of buying a kind of costly house with a mortgage in the next fee atmosphere (or, if they’ve the means, whether or not shopping for a house in money is perhaps applicable!). No matter whether or not a shopper is an aspiring first-time homebuyer or contemplating downsizing in retirement, advisors can add worth by serving to their purchasers navigate increased mortgage-rate environments!