{kind=link}

Firm Overview:

Sula Vineyards Ltd (SVL) is a vineyard and winery positioned within the Nashik area of western India, 180 km northeast of Mumbai. Established in 1999, by Rajeev Samant, SVL was Nashik’s first vineyard and paved the best way for town to turn out to be India’s Wine Capital with nearly 35 different wineries following go well with within the area over the following decade. Sula presently has a manufacturing capability of over 14.5 million litres, of which 12.7 million are housed in Maharashtra and 1.80 million in Karnataka. Sula distributes wines beneath a bouquet of standard manufacturers. Along with the flagship model “Sula,” standard manufacturers embody “RASA,” “Dindori”, “The supply,” “Satori”, “Madera” & “Dia” with its flagship model “Sula” being the “class creator” of wine in India. At present, Sula produces 56 totally different labels of wine at 4 owned and a couple of leased manufacturing services positioned within the Indian states of Maharashtra and Karnataka. The corporate’s distribution platform included over 50 distributors, 11 companies, 14 licensed resellers, 7 firm depots, 3 defence items as of September 30, 2022, over 23,000 factors of sale (together with over 13,500 retail touchpoints and over 9,000 resorts, eating places, and caterers) as of March 31, 2022.

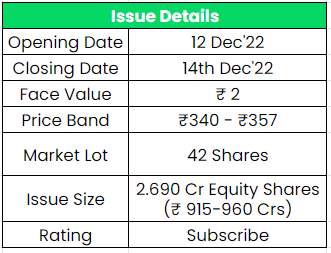

Objects of the Provide:

- To hold out the Provide for Sale of as much as 2,69,00,530 Fairness Shares by the Promoting Shareholders

- Obtain the advantages of itemizing Fairness Shares on the Inventory Exchanges

Funding Rationale:

Market Main Positions: Sula Vineyards Ltd (“Sula”) is India’s largest wine producer and vendor as of March 31, 2022. They’ve been a constant market chief within the Indian wine business when it comes to gross sales quantity and worth (on the idea of the entire income from operations) since Fiscal 2009 crossing 50% market share by worth within the home 100% grapes wine market in Fiscal 2012 to 52% in worth in Fiscal 2022. Moreover, they’re the market chief throughout all 4 value segments, being ‘Elite’ (Rs.950+), ‘Premium’ (Rs.700-950), ‘Economic system’ (Rs.400-700), and ‘Well-liked’ (Rs.400), with a better share of roughly 61% by worth within the ‘Elite’ and ‘Premium’ classes in Fiscal 2022, as in comparison with their total market share of 52% within the Indian wine business. Moreover, they’re additionally acknowledged because the market chief throughout wine variants, together with purple, white, and glowing wines.

Monetary Monitor File: The Income from operations has elevated at a CAGR of twenty-two% from FY11-19. FY21 noticed a decline of 20% YoY in income at Rs.418 crs as a consequence of two most important causes. One is the pandemic and the opposite is the discontinuation of the beer enterprise of their subsidiary firm. FY22 income progress stands at 9% YoY at Rs.454 crs. The phase breakup of FY22: 83.9% of income from personal manufacturers, 7.9% from third-party manufacturers, 7.6% from wine tourism, and 0.6% from others. Gross Margin has improved from 47.8% in FY20 to 65.2%% in FY22. The EBITDA margin has improved from 9.7% in FY20 to 25.6% in FY22. The debt/fairness ratio stands at 0.6x as of FY22.

Robust Clientele: Sula has been a pioneer of wine tourism in India, which has led to a powerful D2C presence. They provide curated experiences, resembling wine-tasting classes, vineyard excursions, and connoisseur eating choices at their wineries, enabling the corporate to construct a stronger reference to their shoppers and popularise wine tourism within the nation. They performed roughly 90,000, 43,000, 85,000, and 59,000 wine-tasting classes throughout Fiscals 2020, 2021, 2022, and the 6 months that ended September 30, 2022, respectively. They’ve elevated the variety of rooms at their Wine Tourism Enterprise services from 33 rooms as of March 31, 2018 to 67 rooms as of September 30, 2022 and plan on including further rooms within the subsequent few years. They proceed to develop their Wine Tourism Enterprise, to construct on their model, expertise, and experience on this enterprise.

Key Dangers:

OFS – The IPO is an entire Provide for Sale (OFS) by the Promoting Shareholders. The Promoting Shareholders will obtain the complete proceeds from the OFS and the Firm is not going to obtain any a part of the proceeds of the Provide. Within the supply on the market (OFS), the promoter Mr. Rajeev Samant is offloading 9,37,203 shares and his stake is reducing from 27.15% to 26.04%. Traders Cofintra S.A, Haystack Investments Restricted, Saama Capital III, Ltd, and some others offloading as much as 2,19,71,700 shares.

Capital Intensive Danger – The corporate’s operations are working capital-intensive in nature with excessive stock as a result of harvest of wine grapes annually in This fall, which is transformed into wines and saved in tanks to be bought within the subsequent months (Q3 is the height gross sales season for the business). Sula extends the 90-120 days credit score interval to state-run companies, who pay after promoting the bottles to their finish clients.

Outlook:

The corporate is within the manufacturing and distribution of wine and the operation of wine tourism venues whereas their listed rivals (Radico Khaitan, United Spirits, and United Breweries) produce alco-beverage merchandise. This differentiates Sula from others and its market-leading place offers the corporate a close to Monopoly standing within the listed area. At a better value band, the itemizing market cap might be round ~Rs.3006 crs and Sula is demanding a P/E a number of of 55x primarily based on FY22 EPS and 47x primarily based on annualized H1FY23 EPS. Whereas evaluating the P/E with its listed friends, the corporate appears to be positioned very near a reasonably valued class. The management place and distinctive product profile supply the corporate some aggressive benefit. Based mostly on the above views, we offer a ‘Subscribe‘ score for this IPO.

In case you are new to FundsIndia, open your FREE funding account with us and revel in lifelong research-backed funding steering.

Different articles chances are you’ll like

Publish Views:

591