{kind=link}

There’s been a number of buzz recently relating to one other 2008 housing disaster unfolding in 2023.

I’m listening to the phrases underwater mortgage and foreclosures once more after greater than a decade.

To make certain, the housing market has cooled considerably since early 2022. There’s no denying that.

You may largely thank a 6% 30-year fixed-rate mortgage for that. Roughly double the three% price you would snag a yr prior.

However this alone doesn’t imply we’re about to repeat historical past.

Goldman Sachs Forecasts 2008 Model Residence Value Drops in 4 Cities

The most recent nugget portending some sort of large actual property market crash comes by way of Goldman Sachs.

The funding financial institution warned that 4 cities might see worth declines of 25% from their 2022 peaks.

These unlucky names embrace Austin, Phoenix, San Diego, and San Jose. All 4 have been sizzling locations to purchase lately.

And it’s just about for that reason that they’re anticipated to see sharp declines. These markets are overheated.

Merely put, house costs obtained too excessive and with mortgage charges now not going for 3%, there was an affordability disaster.

Properties are actually sitting available on the market and sellers are being pressured to decrease their itemizing costs.

A 6.5% Mortgage Price By the Finish of 2023?

In fact, it must be famous that Goldman’s “revised forecast” requires a 6.5% 30-year mounted mortgage for year-end 2023.

It’s unclear when their report was launched, however the 30-year mounted has already trended decrease for the reason that starting of 2023.

For the time being, 30-year mounted mortgages are going for round 6%, or as little as 5.25% if you happen to’re keen to pay a low cost level or two.

And there’s proof that mortgage charges might proceed to enhance because the yr goes on. That is primarily based on inflation expectations, which have brightened recently.

The final couple CPI stories confirmed a decline in client costs, which means inflation might have peaked.

This might put an finish to the Fed’s rate of interest will increase and permit mortgage charges to fall as properly.

Both manner, I consider Goldman’s 6.5% price is just too excessive for 2023. And that may imply their house worth forecast can also be overdone.

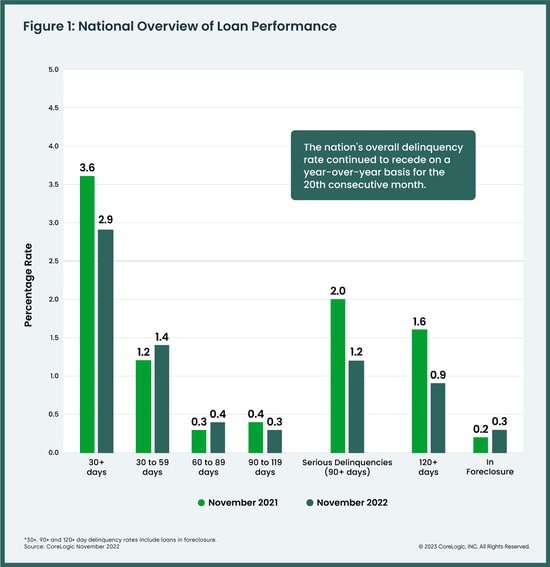

Mortgage Efficiency Stays “Exceptionally Wholesome”

A brand new report from CoreLogic discovered that U.S. mortgage efficiency remained “exceptionally wholesome” as of November 2022.

Simply 2.9% of mortgages have been 30 days or extra delinquent together with these in foreclosures, which is close to document lows.

This represented a 0.7 proportion level lower in contrast with November 2021 when it was 3.6%.

And foreclosures stock (loans at any stage of foreclosures) was simply 0.3%, a slight annual enhance from 0.2% in November 2021.

On the similar time, early-stage delinquencies (30 to 59 days late) have been as much as 1.4% from 1.2% in November 2021.

However on an annual foundation mortgage delinquencies declined for the twentieth straight month.

One huge factor serving to householders is their sizable quantity of house fairness. Total, it elevated

by 15.8% year-over-year within the third quarter of 2022.

That works out to a median achieve of $34,300 per borrower. And the nationwide LTV was just lately under 30%.

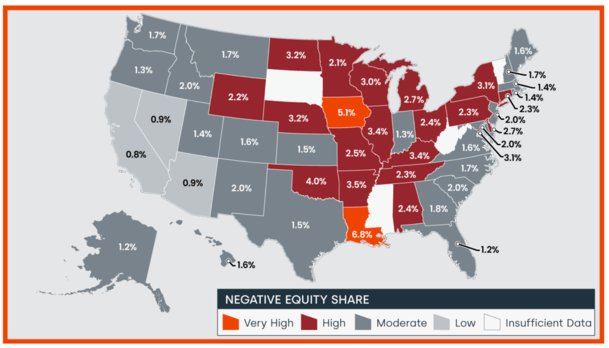

Damaging Fairness Stays Very Low

Through the third quarter of 2022, 1.1 million mortgaged residential properties, or 1.9% of the entire, have been in a detrimental fairness place.

This implies these householders owe extra on their mortgage than the property is at present price.

Again in 2008, these underwater mortgages have been a significant drawback that led to thousands and thousands of quick gross sales and foreclosures.

And whereas detrimental fairness elevated 4% from the second quarter of 2022, it was down 9.8% from the third quarter of 2021.

If downward stress stays on house costs, I do anticipate these numbers to worsen. However contemplating the place we’re at, it’s not 2008 yet again.

Per CoreLogic, detrimental fairness peaked at a staggering 26% of mortgaged residential properties within the fourth quarter of 2009. We’re at 1.9%.

Even when it rises, many owners have mounted rates of interest within the 2-3% vary and little interest in promoting.

Again then, you had each incentive to depart the home and its poisonous adjustable-rate mortgage.

The CFPB Desires Lenders to Make Foreclosures a Final Resort

Again in 2008, there wasn’t a Shopper Monetary Safety Bureau (CFPB). Right now, there may be.

They usually’re being robust on lenders and mortgage servicers that don’t deal with householders proper.

Final week, in addition they launched a weblog submit urging servicers to think about a standard house sale over a foreclosures. That is potential as a result of so many owners have fairness this time round.

However even earlier than it will get to that time, servicers ought to think about a “fee deferral, standalone partial declare, or mortgage modification.”

This permits debtors to remain of their houses, particularly necessary with rents additionally rising.

The principle takeaway right here is that lenders and servicers are going to be closely scrutinized if and once they try to foreclose.

As such, foreclosures ought to stay rather a lot decrease than they did in 2008.

Right now’s Householders Are in A lot Higher Positions Than in 2008

I’ve made this level a number of occasions, however I’ll make it once more.

Even the unlucky house purchaser who bought a property prior to now yr at an inflated worth with a a lot larger mortgage price is healthier off than the 2008 borrower.

We’ll faux their mortgage price is 6.5% and their house worth drops 20% from the acquisition worth.

There’s an excellent likelihood they’ve a 30-year fixed-rate mortgage. In 2008, there was a good higher likelihood that they had an choice ARM. Or some sort of ARM.

Subsequent, we’ll assume our 2022 house purchaser is well-qualified, utilizing absolutely documented underwriting. Which means verifying earnings, belongings, and employment.

Our 2008 house purchaser seemingly certified by way of acknowledged earnings and put zero down on their buy. Their credit score and employment historical past might have additionally been questionable.

The 2022 house purchaser seemingly put down an honest sized down fee too. So that they’ve obtained pores and skin within the recreation.

Our 2022 purchaser can also be properly conscious of the credit score rating injury associated to mortgage lates and foreclosures.

And their property worth will seemingly not drop almost as little as the 2008 purchaser. As such, they may have much less incentive to stroll away.

Finally, many 2008 house consumers had no enterprise proudly owning houses and 0 incentive to remain in them.

Conversely, latest house consumers might have merely bought their properties at non-ideal occasions. That doesn’t equal a housing crash.

If mortgage charges proceed to come back down and settle within the 4/5% vary, it might spell much more reduction for latest consumers and the market total.

Oddly, you would fear about an overheated housing market if that occurs extra so than an impending crash.

After I would fear is that if the unemployment price skyrockets, at which level many owners wouldn’t be capable to pay their mortgages.